Real Estate Depreciation Calculator Guide

Project annual depreciation, tax savings, and cost segregation (per IRS Publication 946) benefits in seconds

Real estate depreciation is one of the most powerful — and most misunderstood — tax advantages available to rental property investors. The IRS allows you to deduct the cost of your investment property over its useful life, even as the property appreciates in market value. This creates a “phantom loss” that reduces your taxable rental income without any actual cash leaving your pocket. Use the free Depreciation Calculator to estimate your annual deductions.

The Real Estate Depreciation Calculator helps investors project annual depreciation deductions, estimate tax savings at their marginal rate, and compare straight-line depreciation against accelerated cost segregation strategies. Whether you own a single rental or a 50-unit portfolio, understanding depreciation is the difference between paying thousands in unnecessary taxes and keeping that money compounding in your next deal.

This depreciation calculator fits into a broader investment analysis workflow. Start with the Rental Property Calculator to project cash flow, use this tool to estimate tax benefits, then check your overall returns in the cash-on-cash calculator Calculator. For BRRRR investors, depreciation impacts your refinance analysis — run both this depreciation calculator and the BRRRR Calculator to see the full picture.

What Is Real Estate Depreciation?

The IRS lets you deduct the cost of your building — even while it gains value

Depreciation is a non-cash tax deduction that allows rental property owners to recover the cost of the building (not the land) over its useful life. For residential rental property, the IRS sets the recovery period at 27.5 years (per IRC Section 168). For commercial property, it’s 39 years. Run the depreciation calculator to see your exact number.

Here’s what makes depreciation unique among tax deductions: it doesn’t require you to spend any money in the current year. Unlike repairs, property management fees, or mortgage interest — which are real cash expenses — depreciation is a paper deduction. You bought the building years ago, but you get to deduct a portion of that cost every year for nearly three decades. Use the depreciation calculator to verify.

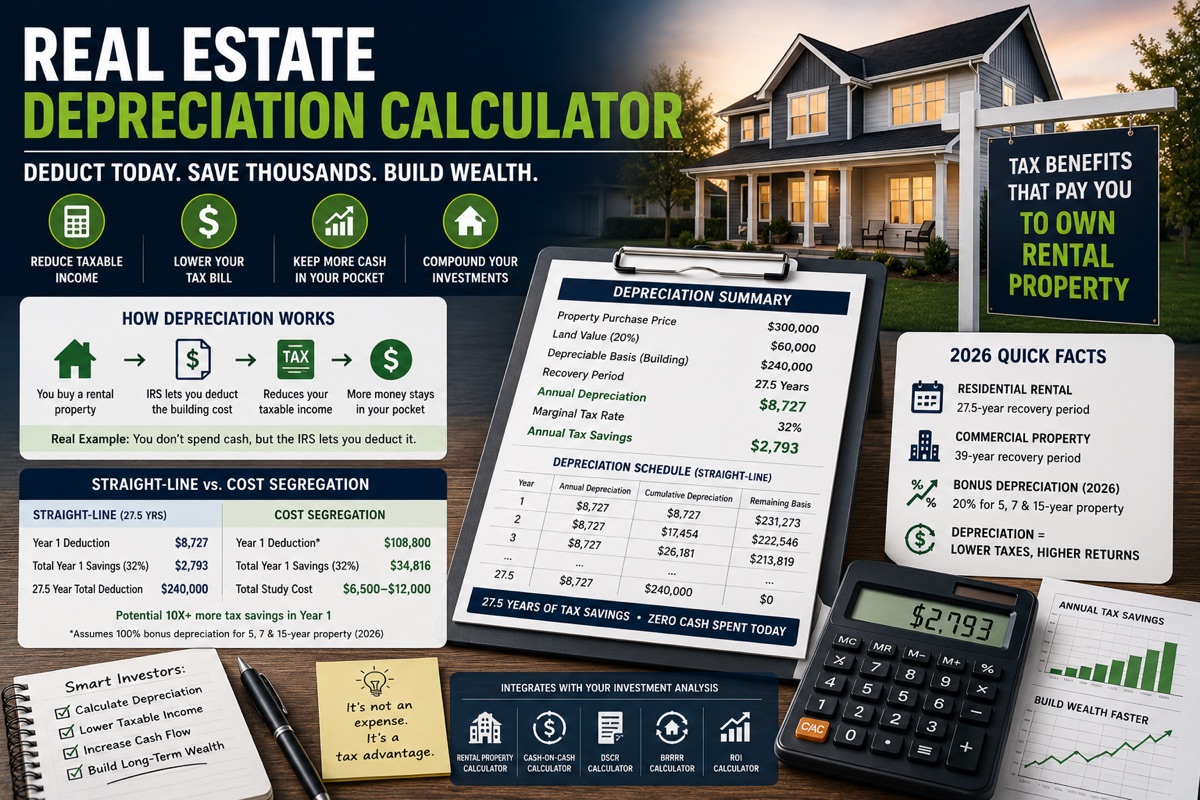

Example: You purchase a rental property for $300,000. The land is worth $60,000 (20% of purchase price). Your depreciable basis is $240,000. Annual straight-line depreciation = $240,000 ÷ 27.5 = $8,727/year. At a 32% marginal tax rate, that’s $2,793 in annual tax savings — money that stays in your pocket, not the IRS’s.

How Residential Rental Depreciation Works (2026 IRS Rules)

27.5-year straight-line: the baseline every investor should know

The Depreciation Formula

Annual Depreciation = (Purchase Price − Land Value) ÷ 27.5

This is straight-line depreciation — the simplest method and the default for residential rental property under IRS Section 168. Every year for 27.5 years, you deduct the same amount. No acceleration, no front-loading, no complexity. The depreciation calculator shows this clearly.

What You Can Depreciate

- The building structure (walls, roof, foundation, plumbing, electrical)

- Capital improvements (new roof, HVAC system, kitchen renovation)

- Closing costs that are part of your basis (title insurance, transfer taxes, recording fees)

What You Cannot Depreciate

- Land — never depreciable, which is why land value allocation matters

- Personal property in the unit (appliances, furniture) — these use different schedules

- Repairs vs. improvements — a repair is a current-year expense, not depreciation

Land Value: The Critical Allocation

The IRS requires you to separate land value from building value. Check with the depreciation calculator before filing. Most investors use one of three methods:

| Method | How It Works | Best For |

|---|---|---|

| Tax Assessor Ratio | Use county’s land/building split from property tax bill | Most common, easiest |

| Appraisal | Professional appraiser allocates land vs. building | High-value or unusual properties |

| 80/20 Rule | Default 80% building, 20% land | Quick estimates, typical suburban |

| Comparable Sales | Land value from recent vacant lot sales nearby | Rural or large-lot properties |

Pro tip: The higher your building allocation, the larger your depreciation deduction. If the tax assessor shows 15% land and your appraiser says 25%, you have a decision to make — but be prepared to defend your allocation in an audit.

How to Use the Real Estate Depreciation Calculator

From purchase price to annual tax savings in four steps

Step 1: Enter Purchase Price and Land Percentage

Start with your actual purchase price — what you paid at closing, including seller credits you received. Land percentage defaults to 20%, which is typical for suburban residential. Urban properties in expensive markets (Manhattan, San Francisco) might have 40-60% land allocation. Rural properties with large lots might also run higher. Use your property tax assessment as a starting point. A quick depreciation calculator run confirms this.

Step 2: Select Property Type

Choose Residential (27.5-year recovery) or Commercial (39-year recovery). Mixed-use properties with residential units above commercial space can be split — depreciate each portion at its respective rate. Most single-family rentals, duplexes, triplexes, and fourplexes are residential. This tool quantifies this deduction.

Step 3: Enter Your Marginal Tax Rate

Your federal marginal tax rate determines how much each dollar of depreciation saves you in taxes. Every the calculator result reflects this rule. Common brackets for real estate investors in 2026:

| Taxable Income (Single) | Marginal Rate |

|---|---|

| $44,726 — $100,375 | 22% |

| $100,376 — $191,950 | 24% |

| $191,951 — $243,725 | 32% |

| $243,726 — $609,350 | 35% |

| Over $609,350 | 37% |

Don’t forget state income tax. A California investor in the 32% federal bracket with 9.3% state rate has an effective marginal rate of 41.3%. That $8,727 depreciation deduction saves $3,604/year instead of $2,793. The calculator applies this automatically.

Step 4: Compare Straight-Line vs. Cost Segregation

Toggle to Cost Segregation mode to see accelerated depreciation. This tool separates your property into component categories with shorter recovery periods:

- 5-year property (15-25% of building): Appliances, carpeting, decorative fixtures, landscaping

- 7-year property (5-10% of building): Office furniture, specialized equipment

- 15-year property (10-20% of building): Land improvements — driveways, sidewalks, fencing, parking lots

- 27.5-year property (remaining): The building structure itself

With 100% bonus depreciation (available through 2026 under current tax law), the 5-year, 7-year, and 15-year components can be deducted in Year 1. This front-loads massive deductions. Plug your numbers into the calculator.

Cost Segregation: The Accelerated Depreciation Strategy

Front-load 30-40% of your depreciation into Year 1

What Is Cost Segregation?

A cost segregation study is an engineering-based analysis that reclassifies building components into shorter depreciation categories. Instead of depreciating your entire building over 27.5 years, a cost seg study identifies components that qualify for 5, 7, or 15-year depreciation — and with bonus depreciation, these shorter-life components can be written off immediately. This tool computes this for your property.

Cost Segregation Example

Property: $400,000 purchase, $80,000 land (20%), $320,000 depreciable basis

| Method | Year 1 Depreciation | Year 1 Tax Savings (32%) |

|---|---|---|

| Straight-Line Only | $11,636 | $3,724 |

| Cost Segregation | $108,800 | $34,816 |

How the cost seg breaks down:

- 5-year property (20% = $64,000): 100% bonus → $64,000 Year 1

- 7-year property (8% = $25,600): 100% bonus → $25,600 Year 1

- 15-year property (15% = $48,000): 100% bonus → $48,000 Year 1

- 27.5-year structure (57% = $182,400): $6,633/year straight-line

- Total Year 1: $64,000 + $25,600 + $48,000 + $6,633 = $144,233

That’s $34,816 in Year 1 tax savings vs. $3,724 with straight-line — a 9.3x improvement. For a high-income investor, this can offset the entire down payment’s tax impact. This is what the calculator reveals.

When Cost Segregation Makes Sense

- Property value over $500,000 — cost seg studies cost $5,000-$15,000, so you need enough basis to justify the fee

- High marginal tax rate (32%+) — bigger rate = bigger dollar savings

- Long hold period (5+ years) — gives you time to benefit before depreciation recapture

- Major renovation — newly placed components qualify for their own depreciation schedules

When It Doesn’t Make Sense

- Properties under $200,000 — the study fee eats too much of the benefit

- Low tax bracket (12-22%) — savings may not justify the cost

- Short hold (under 3 years) — depreciation recapture at sale cancels much of the benefit

- Already in a loss position — passive loss limitations may prevent you from using the deduction

Depreciation Recapture: What Happens When You Sell

The IRS wants its cut back — but there are legal ways to defer

How Recapture Works

When you sell a depreciated property, the IRS “recaptures” the depreciation you claimed by taxing it at a special rate. For residential rental property, depreciation recapture is taxed at 25% — regardless of your ordinary income tax bracket. That is exactly what the calculator is for.

Example: You claimed $87,270 in total depreciation over 10 years. When you sell, the IRS taxes that amount at 25% = $21,818 in recapture tax, on top of any capital gains tax on appreciation.

Strategies to Manage Recapture

1031 exchange calculator — Defer both capital gains AND depreciation recapture by exchanging into a like-kind property. The 1031 Exchange Calculator shows an estimate of how much you save.

Die and Step Up — Morbid but effective. At death, heirs receive a stepped-up basis, eliminating both capital gains and depreciation recapture. This is why many investors hold forever and refinance instead of selling.

Installment Sale — Spread the gain over multiple years to stay in lower brackets, reducing the effective tax rate on the recapture portion.

Opportunity Zone Investment — Reinvest capital gains into a Qualified Opportunity Zone fund for potential tax deferral and exclusion.

Passive Loss Rules and Real Estate Professional Status

Who can actually use depreciation deductions — and when

The $25,000 Allowance

Most rental property owners face passive activity loss rules. Rental income is generally “passive,” and passive losses can only offset passive income. This tool breaks this down year by year. However, the IRS provides a $25,000 special allowance for active participants in rental real estate:

- AGI under $100,000: Full $25,000 allowance

- AGI $100,000-$150,000: Phased out ($1 reduction per $2 of AGI over $100K)

- AGI over $150,000: No allowance — passive losses carry forward

Real Estate Professional Status (REPS)

If you qualify as a Real Estate Professional, rental losses become non-passive — meaning you can deduct them against W-2 income, business income, and any other income. Your the calculator output depends on this. Requirements:

- 750+ hours/year in real estate activities

- More than 50% of your total working hours in real estate

- Material participation in each rental activity (or elect to aggregate)

REPS combined with cost segregation is the most powerful tax strategy in real estate. A qualifying investor with a $500,000 property can generate $100,000+ in Year 1 deductions against ordinary income.

Depreciation for Different Property Types

Recovery periods, methods, and special rules by property category

| Property Type | Recovery Period | Method | Annual Rate |

|---|---|---|---|

| Residential Rental (1-4 units) | 27.5 years | Straight-Line | 3.636% |

| Residential Rental (5+ units) | 27.5 years | Straight-Line | 3.636% |

| Commercial (office, retail) | 39 years | Straight-Line | 2.564% |

| Land Improvements | 15 years | 150% DB/SL | Varies |

| Personal Property (appliances) | 5 years | 200% DB/SL | Varies |

| Qualified Improvement Property | 15 years | Straight-Line | 6.667% |

Key distinction: Residential means tenants live there (apartments, houses, duplexes). Commercial means business use (office buildings, warehouses, retail). A mixed-use building splits based on square footage allocation.

Common Depreciation Mistakes Investors Make

Avoid these errors that trigger audits or leave money on the table

Mistake 1: Depreciating Land

Land is never depreciable. If you depreciate 100% of your purchase price, the IRS will disallow the land portion and assess penalties. Always allocate land separately — typically 15-30% of purchase price for suburban residential. Run this tool to see your exact number.

Mistake 2: Missing the Placed-in-Service Date

Depreciation starts when the property is “placed in service” — available and ready for rent, not when you close. If you buy in June but spend three months renovating, depreciation starts in September. The first-year deduction is prorated by month. Use the calculator to verify.

Mistake 3: Confusing Repairs with Improvements

A repair maintains the property in its current condition (fixing a leaky faucet, patching drywall) and is deducted in full in the current year. An improvement adds value or extends useful life (new roof, kitchen remodel) and must be depreciated over 27.5 years. The IRS safe harbor allows expensing items under $2,500 each (the de minimis rule). The calculator shows this clearly.

Mistake 4: Forgetting Closing Costs in Basis

Your depreciable basis isn’t just the purchase price. Add: title insurance, recording fees, transfer taxes, legal fees, and survey costs. Subtract: seller credits received. These additions increase your annual depreciation deduction. Check with this tool before filing.

Mistake 5: Not Claiming Depreciation

Here’s the catch — the IRS requires you to reduce your basis by the depreciation you could have claimed, whether or not you actually claimed it. If you skip depreciation for years, you still owe recapture tax on the phantom deductions when you sell. There is zero benefit to not claiming depreciation.

Depreciation and the BRRRR Strategy

How depreciation supercharges Buy-Rehab-Rent-Refinance-Repeat

BRRRR investors get a unique depreciation advantage. When you refinance at the after-repair value (ARV), your depreciable basis includes the purchase price plus renovation costs — potentially creating a much larger depreciation deduction than the original purchase would suggest.

BRRRR Example:

- Purchase price: $150,000 (land: $30,000)

- Renovation: $50,000 (all depreciable — improvements to building)

- Depreciable basis: $120,000 + $50,000 = $170,000

- Annual depreciation: $170,000 ÷ 27.5 = $6,182/year

- ARV after renovation: $250,000

- Cash-out refinance at 75% LTV: $187,500 loan

The renovation costs increase your depreciable basis even though you recovered your cash through refinancing. You’re depreciating money you already got back — one of the reasons BRRRR is so tax-efficient.

Use the BRRRR Calculator to model the full cycle, then this the calculator to project the tax benefits.

2026 Bonus Depreciation Update

What investors need to know about the phase-down

Bonus depreciation — the provision that lets you deduct 100% of short-life property in Year 1 — has been phasing down since 2023:

| Tax Year | Bonus Depreciation Rate |

|---|---|

| 2022 | 100% |

| 2023 | 80% |

| 2024 | 60% |

| 2025 | 40% |

| 2026 | 20% |

| 2027+ | 0% (unless extended) |

What this means for 2026: If a cost segregation study identifies $100,000 in 5/7/15-year property, you can deduct only $20,000 in Year 1 as bonus depreciation. The remaining $80,000 follows the regular MACRS schedule for each asset class. This significantly reduces the Year 1 benefit compared to 2022-2023.

Legislative watch: Multiple proposals in Congress aim to restore 100% bonus depreciation. The Tax Cuts and Jobs Act extension and the bipartisan ALIGN Act both include provisions to reinstate full bonus. Check with your CPA for current status.

Strategy shift: With lower bonus percentages, cost segregation studies need higher property values to justify the study cost. The break-even point has shifted from roughly $300,000 to $500,000+ for most investors in 2026.

How Depreciation Affects Your Real Return

The metric most investors ignore when comparing deals

When comparing two rental properties, most investors look at cap rate calculator, cash-on-cash return, and NOI. But depreciation creates a “tax-adjusted return” that can flip the ranking of two deals.

Deal A: $200,000, 7% cap rate, $14,000 NOI

- Depreciation: $5,818/year

- Tax savings (32%): $1,862/year

- Tax-adjusted NOI: $15,862

- Tax-adjusted cap rate: 7.93%

Deal B: $350,000, 6.5% cap rate, $22,750 NOI

- Depreciation: $10,182/year

- Tax savings (32%): $3,258/year

- Tax-adjusted NOI: $26,008

- Tax-adjusted cap rate: 7.43%

Deal A still wins on tax-adjusted cap rate, but the gap narrows from 0.50% to 0.50%. For deals closer in raw cap rate, depreciation can flip the winner — especially when one property has a higher building-to-land ratio.

Calculate your tax-adjusted returns using the Cap Rate Calculator alongside this depreciation tool.

Depreciation for Short-Term Rentals (Airbnb/VRBO)

Different rules, different opportunities

Short-term rentals (average stay under 7 days) are not considered “rental activity” under IRS passive activity rules — they’re treated as a business. This creates unique depreciation opportunities:

- No REPS required: Material participation in an STR makes losses non-passive automatically

- Full cost segregation benefit: STR owners can use accelerated depreciation against active income

- Self-employment tax: STR income may be subject to SE tax (15.3%), but depreciation reduces the taxable amount

- Average stay matters: If your average guest stay exceeds 7 days, the property reverts to standard rental passive activity rules

Many high-income professionals (doctors, attorneys, tech workers) use STR properties with cost segregation as their primary tax reduction strategy. A $600,000 STR with a cost seg study can generate $150,000+ in Year 1 deductions against W-2 income — no REPS qualification needed.

Frequently Asked Questions About Real Estate Depreciation

Can I depreciate a property I live in part-time?

Only the rental-use portion. If you rent a property 9 months and use it personally for 3 months, you can depreciate 75% of the building value. The personal-use portion is not depreciable. Second homes rented fewer than 14 days/year have no rental income to report — and no depreciation.

What happens if I convert my primary residence to a rental?

Your depreciable basis is the lower of your adjusted basis (what you paid, plus improvements, minus any casualty losses) or the fair market value at conversion. If your home appreciated, you don’t get to depreciate the gain — only your original cost basis. Depreciation starts on the conversion date.

Can I take depreciation if the property has negative cash flow?

Yes. Depreciation is based on your cost basis, not your cash flow. A property producing negative cash flow still generates depreciation deductions. However, passive loss rules may limit when you can use those deductions — they may need to carry forward until you have passive income or sell the property.

How does depreciation work for a 1031 exchange property?

The replacement property’s depreciable basis equals the relinquished property’s remaining basis plus any additional cash (boot) you invested. You don’t get a fresh 27.5-year schedule on the carried-over basis — it continues from where the old property left off. Only the boot portion starts a new 27.5-year clock.

Is there a limit to how many properties I can depreciate?

No limit. You can depreciate every rental property you own simultaneously. Each property has its own depreciation schedule based on its placed-in-service date and cost basis.

What records do I need to keep for depreciation?

Keep purchase documents (HUD-1/closing disclosure), property tax assessments (for land allocation), records of capital improvements with dates and costs, cost segregation studies, and Form 4562 from each year’s tax return. The IRS can audit depreciation claims for up to 3 years after filing (6 years if income is underreported by 25%+).

Can I claim depreciation on a property held in an LLC?

Yes. The LLC is a pass-through entity — depreciation flows through to the members’ personal tax returns (or the LLC’s return if it elects corporate taxation). The entity type doesn’t affect depreciation calculations.

Should I do a cost segregation study on a property I’ve owned for years?

Yes — it’s called a “look-back” cost segregation study. You can catch up on missed accelerated depreciation by filing Form 3115 (Change in Accounting Method) for a “catch-up” deduction in the current year. No need to amend prior returns.

How does depreciation affect my property’s basis for capital gains?

Every dollar of depreciation reduces your adjusted basis. When you sell, capital gain = sale price − adjusted basis − selling costs. Lower basis = higher gain = more tax. This is depreciation recapture in action. Even if you didn’t claim depreciation, the IRS assumes you did (or should have).

What’s the difference between depreciation and amortization in real estate?

Depreciation applies to tangible property (buildings, improvements). Amortization applies to intangible assets (loan origination fees, goodwill, lease acquisition costs). Both reduce taxable income over time, but they follow different IRS schedules and rules.

Start Calculating Your Depreciation Tax Savings

Understanding depreciation is essential for every rental property investor — it’s free money the IRS gives you for owning real estate. Use the this tool to project your annual deduction from the calculator, compare straight-line vs. cost segregation, and estimate your tax savings at your specific marginal rate.

Pair it with the NOI Calculator for operating income, the Cash-on-Cash Calculator for return on invested capital, and the DSCR Calculator for lender qualification — the full toolkit for making data-driven investment decisions.

Disclaimer: This article is for educational purposes only and does not constitute financial, investment, legal, or tax advice. Real estate investing involves significant risk, including the potential loss of capital. All numbers, rates, and projections are illustrative examples and may not reflect your specific situation. Consult qualified financial, legal, and tax professionals before making any investment decisions.

Leave a Reply