Selling a rental property without running the tax numbers first is how investors lose $30,000 or more to Uncle Sam. This capital gains tax calculator shows you exactly what you’ll owe in federal tax, state tax, depreciation recapture, and NIIT — then tells you how much cash you actually keep after the sale. Most sellers fixate on the sale price. The investors who build real wealth? They calculate the after-tax number before they ever list the property. Use the free Capital Gains Tax Calculator to run your own numbers.

Consider a real scenario. You bought a duplex in Phoenix for $320,000 in 2019, claimed $52,000 in depreciation, and now you’re selling for $485,000. Your total gain looks like $165,000 — but the tax picture is more complicated than that. Depreciation recapture alone hits you at 25%, costing $13,000 on the recaptured amount. Federal long-term capital gains add another layer. State taxes in Arizona take 2.5%. And if your modified adjusted gross income exceeds $200,000, the 3.8% Net Investment Income Tax (NIIT) kicks in too. Without a capital gains tax calculator, you’re guessing at the number that matters most: cash after tax.

This article walks through how the calculator works, what each tax component means, where investors get surprised, and how to evaluate whether selling, holding, or doing a 1031 exchange makes the most financial sense. Whether you own one rental in Memphis or twelve units across three states, the math here applies to every disposition decision you’ll face.

On This Page

- What Is Capital Gains Tax on Real Estate?

- How to Calculate Capital Gains Tax (Step by Step)

- How to Use the Capital Gains Tax Calculator

- 2026 Capital Gains Tax Rates

- Depreciation Recapture: The Tax Most Investors Forget

- Net Investment Income Tax (NIIT)

- State Capital Gains Taxes

- Worked Example: Selling a $485K Rental in Phoenix

- Sell vs Hold vs 1031 Exchange

- Mistakes That Increase Your Tax Bill

- Understanding Tax Drag

- Limitations of This Calculator

- Frequently Asked Questions

- Related Calculators

What Is Capital Gains Tax on Real Estate?

The tax on profit when you sell an investment property

Capital gains tax is the federal tax you pay on the profit from selling a property. The IRS defines the gain as the difference between your net sale price and your adjusted basis. Sounds straightforward, but “adjusted basis” is where things get tricky — because it accounts for purchase costs, capital improvements, and depreciation you’ve claimed over the years. Run the capital gains tax calculator to see your exact number.

For real estate investors, capital gains tax has multiple components. Tthe federal long-term capital gains tax (0%, 15%, or 20% depending on income). There’s depreciation recapture taxed at up to 25%. There’s state-level capital gains tax, which varies wildly — from 0% in Texas and Florida to 13.3% in California. And tthe Net Investment Income Tax (NIIT) at 3.8% for high earners. Each piece gets calculated separately, and they all stack on top of each other. Use the capital gains tax calculator to verify.

A capital gains tax calculator pulls all these components together into one number: your total estimated tax liability. More importantly, it shows you the number that actually matters — how much cash you reconsider the assumptions with after paying everything. That after-tax figure is what should drive your sell-or-hold decision, not the gross sale price.

How to Calculate Capital Gains Tax (Step by Step)

The five-step formula every investor should understand

Before you plug numbers into the capital gains tax calculator, it helps to understand the underlying math. The IRS treats real estate capital gains differently from stock gains because of depreciation. Here’s the formula broken down into five steps:

| Step | Formula | What It Means |

|---|---|---|

| 1. Adjusted Basis | Purchase Price + Closing Costs + Improvements – Depreciation | Your true cost basis after adjustments |

| 2. Net Sale Price | Sale Price – Selling Costs | What you actually receive from the sale |

| 3. Total Gain | Net Sale Price – Adjusted Basis | Your taxable profit |

| 4. Depreciation Recapture Tax | Depreciation Claimed x 25% | Tax on previously deducted depreciation |

| 5. Remaining Gain Tax | (Total Gain – Depreciation) x CG Rate + State Tax + NIIT | Federal, state, and NIIT on the remaining gain |

The key insight here is that depreciation gets taxed at a higher rate than the rest of your gain. While long-term capital gains typically face a 15% or 20% rate, depreciation recapture is taxed at up to 25% under Section 1250 of the Internal Revenue Code. This means an investor who claimed $80,000 in depreciation over seven years could owe $20,000 in recapture tax alone — before the regular capital gains tax even enters the picture. The capital gains tax calculator shows this clearly.

One thing that trips up investors constantly: mortgage payoff does not reduce your taxable gain. Your mortgage balance affects how much cash you receive, but it has zero impact on the tax calculation. The IRS doesn’t care how much you still owe the bank. They care about the difference between what you sold the property for and your adjusted basis. The capital gains tax calculator separates these clearly so you can see both your tax liability and your actual cash proceeds.

How to Use the Capital Gains Tax Calculator

From inputs to after-tax cash in 60 seconds

Step 1: Enter your purchase details

Start with your original purchase price — the amount you paid for the property, not its current market value. Then add any purchase closing costs that were capitalized (title insurance, transfer taxes, attorney fees). Finally, enter the total dollar amount of capital improvements you’ve made since buying. Capital improvements include things like a new roof, HVAC replacement, kitchen remodel, or added square footage. Routine maintenance and repairs don’t count. A quick this tool check confirms this.

Step 2: Enter accumulated depreciation

This is the total depreciation you’ve claimed on your tax returns since you bought the property. For residential rental property, the IRS allows straight-line depreciation over 27.5 years. If you bought a $300,000 property (with $60,000 allocated to land), you’ve been depreciating $240,000 over 27.5 years — roughly $8,727 per year. After 7 years, that’s about $61,091 in accumulated depreciation. If you’re unsure, check your Schedule E or ask your CPA. The Depreciation Calculator can help you estimate this figure. The calculator computes this instantly.

Step 3: Enter sale price and selling costs

Enter the expected sale price based on recent comps in your market. For selling costs, include agent commissions (typically 5%–6% of sale price), transfer taxes, title fees, and any seller concessions. On a $485,000 sale, expect selling costs between $24,250 and $33,950. These costs reduce your net sale price, which reduces your taxable gain. Plug your numbers into this tool.

Step 4: Set your tax rates

Enter your federal capital gains rate — most investors fall in the 15% bracket. High earners above $518,900 (single) or $583,750 (married filing jointly) in 2026 pay 20%. Add your state tax rate if applicable. Toggle the NIIT on if your modified adjusted gross income exceeds $200,000 (single) or $250,000 (married). The calculator treats each of these as separate line items so you see where every dollar goes.

Step 5: Review total tax and cash after tax

The calculator outputs your total estimated tax, broken into depreciation recapture, federal capital gains, state tax, and NIIT. It also shows cash before tax (net sale price minus mortgage payoff) and cash after tax (what you actually pocket). The tax drag percentage tells you how much of your gain goes to taxes — a critical metric for comparing sell vs. hold vs. 1031 exchange scenarios. The tax calculator breaks this down for you.

2026 Capital Gains Tax Rates

Federal brackets, recapture rates, and the NIIT threshold

Capital gains tax rates in 2026 depend on your filing status and taxable income. For most real estate investors selling rental property, the 15% bracket applies. The current federal long-term capital gains rates, based on IRS Topic 409:

| Tax Rate | Single Filer | Married Filing Jointly |

|---|---|---|

| 0% | Up to $48,350 | Up to $96,700 |

| 15% | $48,351 – $518,900 | $96,701 – $583,750 |

| 20% | Over $518,900 | Over $583,750 |

These rates apply only to long-term capital gains — property held longer than one year. If you sell within 12 months of purchase, the gain is treated as short-term and taxed at your ordinary income rate, which could be as high as 37%. That’s a massive difference. An investor with $100,000 in gain pays $15,000 at the long-term rate but up to $37,000 at short-term rates. The holding period matters enormously. Every the calculator result reflects this.

On top of the federal rate, depreciation recapture is taxed separately at a maximum of 25%. And the 3.8% NIIT applies to investment income for high earners. So the worst-case effective federal rate on a rental property sale could reach 23.8% (20% capital gains + 3.8% NIIT) on the regular gain, plus 25% on the recaptured depreciation. Layer state taxes on top, and some investors in states like California or New York face combined rates above 35%.

The capital gains tax calculator handles all of these layers automatically. You enter your rates, and it separates each component so you see the exact contribution of federal tax, recapture, state tax, and NIIT to your total bill.

Depreciation Recapture: The Tax Most Investors Forget

You deducted it on the way up; the IRS takes it back on the way out

Depreciation recapture is the portion of your gain that represents previously deducted depreciation. While you owned the property, you claimed depreciation as an expense that reduced your taxable rental income. When you sell, the IRS “recaptures” that benefit by taxing the depreciation amount at a special rate of up to 25%.

Why it catches people off guard. Suppose you bought a rental in Austin for $350,000 in 2018 and claimed $76,000 in depreciation over 8 years. Your adjusted basis drops from $350,000 to $274,000. When you sell for $450,000 (after selling costs), your total gain is $176,000. But the first $76,000 of that gain — the depreciation — gets taxed at 25%, not your regular capital gains rate. That’s $19,000 in recapture tax before you even get to the capital gains calculation on the remaining $100,000.

Many investors don’t realize they owe recapture tax even if the property’s value didn’t actually increase. Imagine a scenario where property values stayed flat. You bought for $350,000 and sell for $350,000. Your gain looks like zero. But because you claimed $76,000 in depreciation, your adjusted basis is $274,000 — meaning you have a $76,000 taxable gain entirely from recapture. You owe roughly $19,000 in taxes on a property that didn’t appreciate at all.

The capital gains tax calculator separates depreciation recapture from regular capital gains tax so you can see both amounts independently. If your recapture tax looks high, that’s a signal to explore a 1031 exchange, which can defer both recapture and capital gains taxes if you reinvest the proceeds into a qualifying replacement property.

Net Investment Income Tax (NIIT)

The 3.8% surcharge high earners can’t avoid

The Net Investment Income Tax adds 3.8% to your capital gains tax if your modified adjusted gross income (MAGI) exceeds $200,000 for single filers or $250,000 for married filing jointly. This threshold has not been adjusted for inflation since the NIIT was introduced in 2013, so it catches more taxpayers every year.

The NIIT applies to the lesser of your net investment income or the amount by which your MAGI exceeds the threshold. For most real estate investors selling a property with a six-figure gain, the NIIT applies to the entire gain amount. On a $150,000 capital gain, that’s $5,700 in additional tax.

This calculator estimates NIIT as an upper-bound figure — 3.8% of your total gain when toggled on. Your actual NIIT may be lower depending on your full income picture and deductions. However, for planning purposes, assuming the full 3.8% gives you a conservative (higher) tax estimate, which is smarter than underestimating and getting surprised at filing time. If NIIT pushes your total tax into uncomfortable territory, discuss strategies with a tax professional before selling.

State Capital Gains Taxes

Zero in some states, devastating in others

State capital gains taxes range from 0% to over 13%, and they stack on top of your federal liability. This is where the geographic location of your property — or your personal tax residence — significantly impacts your after-tax proceeds.

| State | Capital Gains Tax Rate | Notes |

|---|---|---|

| Texas | 0% | No state income tax |

| Florida | 0% | No state income tax |

| Tennessee | 0% | No state income tax on earned or capital gains |

| Arizona | 2.5% | Flat income tax rate |

| Colorado | 4.4% | Flat income tax rate |

| New York | Up to 10.9% | Progressive; NYC adds 3.876% |

| California | Up to 13.3% | Treats capital gains as ordinary income |

The difference is staggering. An investor selling a rental property with $200,000 in capital gains pays $0 in state tax in Texas but up to $26,600 in California. That’s $26,600 more in tax on the exact same gain — enough to fund a down payment on the next investment property.

The capital gains tax calculator uses a flat state tax rate input for simplicity. Actual state tax rules vary considerably — some states have progressive brackets, some offer exclusions for certain property types, and a few tax capital gains at lower rates than ordinary income. The calculator gives you a solid estimate, but investors in high-tax states should confirm their specific rate with a CPA before making disposition decisions.

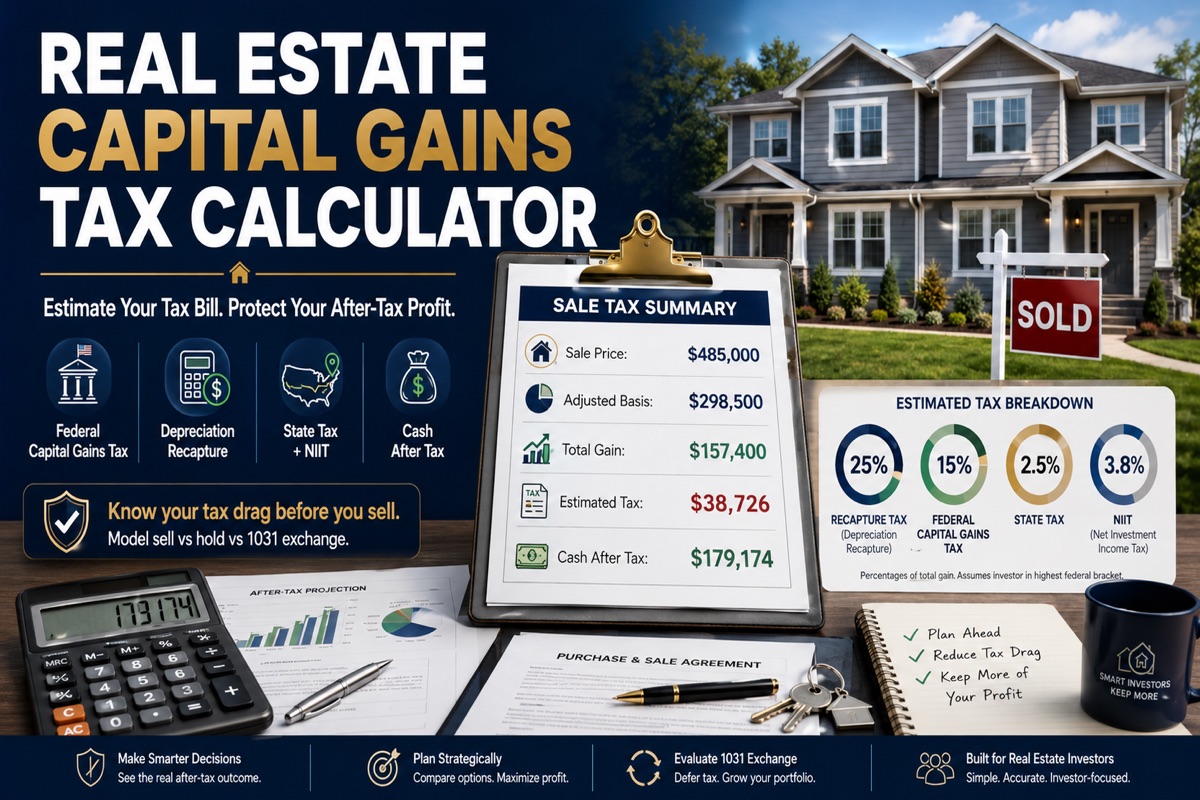

Worked Example: Selling a $485K Rental in Phoenix

Real numbers from a realistic scenario

Let’s revisit the Phoenix duplex from the introduction and run it through the capital gains tax calculator step by step.

Property Details:

- Purchased in 2019 for $320,000

- Purchase closing costs: $8,500

- Capital improvements (new HVAC, roof repair): $22,000

- Accumulated depreciation over ~7 years: $52,000

- Sale price: $485,000

- Selling costs (6%): $29,100

- Remaining mortgage balance: $238,000

Capital Gains Tax Calculator Outputs:

| Line Item | Amount |

|---|---|

| Adjusted Basis | $298,500 ($320K + $8.5K + $22K – $52K) |

| Net Sale Price | $455,900 ($485K – $29.1K) |

| Total Gain | $157,400 |

| Depreciation Recapture Tax (25%) | $13,000 |

| Federal CG Tax on Remaining Gain (15%) | $15,810 |

| Arizona State Tax (2.5%) | $3,935 |

| NIIT (3.8%, if applicable) | $5,981 |

| Total Estimated Tax | $38,726 |

| Cash Before Tax | $217,900 ($455.9K – $238K mortgage) |

| Cash After Tax | $179,174 |

| Effective Tax Rate | 24.6% of total gain |

| Tax Drag | 17.8% of cash before tax |

That $38,726 tax bill is the kind of number that changes decisions. The investor walks away with $179,174 in after-tax cash — not the $217,900 they might have mentally expected. The 17.8% tax drag is in the moderate range, which means this sale is reasonable but worth comparing against alternatives.

Notice how mortgage payoff ($238,000) reduces cash but doesn’t affect the gain or tax calculation at all. An investor with a $100,000 mortgage would owe the same $38,726 in tax — they’d just receive more cash at closing. This is one of the most misunderstood aspects of real estate tax accounting.

Sell vs Hold vs 1031 Exchange

Using tax drag to make smarter disposition decisions

The capital gains tax calculator gives you a verdict based on your tax drag ratio — the percentage of your pre-tax cash that goes to taxes. This metric helps you evaluate whether selling outright makes sense or whether you should consider alternatives.

| Tax Drag Level | What It Means | Suggested Action |

|---|---|---|

| Low (under 10%) | Tax is a small share of equity | Strong after-tax liquidity; sell if it fits your strategy |

| Moderate (10%–25%) | Meaningful but manageable tax | Compare selling vs. holding vs. 1031 |

| High (25%–40%) | Tax consumes significant equity | Seriously consider a 1031 exchange or timing the sale |

| Severe (over 40%) | Tax takes a large share of equity | 1031 exchange strongly recommended; consult a CPA |

A 1031 exchange lets you defer both capital gains tax and depreciation recapture by reinvesting sale proceeds into a like-kind replacement property. In our Phoenix example, the investor could defer the entire $38,726 tax bill by identifying a replacement property within 45 days and closing within 180 days. That’s $38,726 that stays invested and compounding rather than going to the IRS. Use the 1031 Exchange Calculator to model this scenario.

However, a 1031 exchange isn’t always the right move. It restricts your reinvestment options, requires a qualified intermediary, and defers the tax rather than eliminating it. If the tax drag is low and you want maximum flexibility with your proceeds, selling outright might be the smarter play. This tool gives you the data to make that call based on numbers, not gut feeling.

Mistakes That Increase Your Tax Bill

Six errors that cost real estate investors real money

1. Forgetting to add capital improvements to basis

Every dollar of capital improvement increases your adjusted basis, which reduces your taxable gain. A $35,000 kitchen remodel you forgot to include means $35,000 more in taxable gain — potentially $5,250+ in additional federal tax. Keep receipts for every improvement. The IRS distinguishes between improvements (which add to basis) and repairs (which don’t). A new roof is an improvement. Patching a leak is a repair.

2. Ignoring depreciation recapture

Some investors calculate their capital gains tax using only the 15% long-term rate and forget that depreciation recapture is taxed at 25%. On $80,000 of accumulated depreciation, that oversight means underestimating your tax bill by $8,000 (the difference between 25% and 15% on $80,000). The capital gains tax calculator always separates recapture from regular gains precisely to prevent this error.

3. Thinking mortgage payoff reduces your tax

This is probably the single most common misconception in real estate investing. Your mortgage balance affects your cash proceeds — not your taxable gain. Whether you owe $300,000 or $0 on the mortgage, your capital gains tax is identical. The calculator shows both figures side by side so you can see the distinction clearly.

4. Missing the short-term holding period cutoff

If you sell a property you’ve owned for less than 12 months, the gain is taxed as ordinary income — at rates up to 37% instead of 15%–20%. An investor who flips a property in 11 months with a $120,000 gain could owe $44,400 at the 37% rate instead of $18,000 at 15%. That’s a $26,400 difference for holding 30 days too few. Always check your holding period before listing.

5. Not accounting for state taxes

Federal tax gets all the attention, but state taxes add 2%–13% to your effective rate depending on location. An investor in Portland, Oregon (9.9% state rate) selling with $200,000 in gains owes an extra $19,800 in state tax that a federal-only estimate would completely miss.

6. Overlooking the NIIT threshold

The 3.8% NIIT sneaks up on investors who cross the $200,000/$250,000 MAGI threshold. On a $180,000 gain, that’s $6,840 you didn’t budget for. The threshold hasn’t been inflation-adjusted since 2013, so more investors hit it every year. Toggle NIIT on in the calculator if you’re anywhere near the threshold — better to overestimate than get caught short.

Understanding Tax Drag

The metric that separates good sales from bad ones

Tax drag measures how much of your pre-tax cash equity gets consumed by taxes. It’s expressed as a percentage: total tax divided by cash before tax. This single number tells you more about the quality of a sale than the gross gain or the sale price ever could.

A tax drag of 8% means you keep 92 cents of every dollar. That’s strong after-tax liquidity. A tax drag of 35% means you lose more than a third of your equity to taxes — and at that level, you should seriously question whether selling is the right move at all.

Tax drag varies widely based on four factors: how much depreciation you’ve claimed, your combined federal and state rates, whether NIIT applies, and how much use you carry. Ironically, investors who benefited most from depreciation deductions during ownership face the highest recapture tax at sale. The depreciation giveth, and the depreciation taketh away.

When the capital gains tax calculator returns a tax drag verdict of “HIGH” or “SEVERE,” that’s your cue to model alternative scenarios. Run the numbers with a 1031 exchange. Check whether holding the property for another 2–3 years changes the math. Compare the after-tax cash from selling against the ongoing cash flow from keeping the rental. The Real Estate ROI Calculator can help you model the hold scenario.

Limitations of This Calculator

What it estimates and what it can’t tell you

This capital gains tax calculator provides a realistic estimate of your total tax liability and after-tax cash proceeds from selling an investment property. It’s built for planning and decision-making — not for filing taxes. What it does not cover:

- Primary residence exclusion: If the property was your primary home for at least 2 of the last 5 years, you may qualify for the Section 121 exclusion ($250,000 single / $500,000 married). This calculator is designed for investment property and does not apply the exclusion automatically.

- Partial year depreciation: The calculator uses the depreciation amount you enter. It does not compute partial-year adjustments for the year of sale. Your CPA will handle the final-year proration.

- Installment sales: If you sell with seller financing, the gain may be recognized across multiple tax years. This calculator assumes a standard sale with proceeds received in the year of closing.

- State-specific rules: State taxes are calculated using a flat rate input. Some states have progressive brackets, exemptions, or special treatment for real estate gains. California, for instance, treats capital gains as ordinary income with rates up to 13.3%.

- 1031 exchange eligibility: The calculator does not determine whether your sale qualifies for a 1031 exchange. That requires meeting specific IRS rules around like-kind property, timelines, and qualified intermediaries.

All outputs are estimates, not tax advice. Before making any disposition decision, confirm your tax liability with a licensed CPA or tax attorney who understands real estate. Tax rules change, and individual circumstances — like passive activity loss carryovers, net operating losses, or qualified opportunity zone investments — can significantly alter your actual tax bill.

Frequently Asked Questions

Common questions about real estate capital gains tax

What is a capital gains tax calculator?

A capital gains tax calculator estimates the federal, state, and additional taxes you owe when selling an investment property. You enter your purchase price, improvements, depreciation, sale price, and tax rates. The calculator outputs your total gain, depreciation recapture tax, federal capital gains tax, state tax, NIIT (if applicable), and the after-tax cash you’ll actually receive. It’s a planning tool that helps you decide whether to sell outright, hold, or pursue a 1031 exchange.

What is depreciation recapture?

Depreciation recapture is a tax on depreciation deductions you previously claimed during ownership. Rental property owners deduct depreciation each year against rental income. When the property sells, the IRS recaptures those deductions by taxing the depreciated amount at a rate of up to 25%. For example, if you claimed $60,000 in depreciation over 7 years, you could owe up to $15,000 in recapture tax at the time of sale — regardless of whether the property actually increased in value.

Does paying off my mortgage reduce my capital gains tax?

No. This is one of the most widespread myths in real estate investing. Your mortgage balance has zero effect on your taxable gain. The IRS calculates capital gains based on sale price minus adjusted basis. Your mortgage is a financing arrangement — it affects how much cash you receive at closing, but it doesn’t change the tax owed. An investor who sells a $500,000 property with a $400,000 mortgage owes the exact same capital gains tax as one who owns the same property free and clear.

What’s the difference between short-term and long-term capital gains?

Short-term capital gains apply to properties held for one year or less and are taxed at your ordinary income rate — up to 37% in 2026. Long-term capital gains apply to properties held longer than one year and are taxed at 0%, 15%, or 20% depending on income. The holding period is calculated from your purchase closing date to your sale closing date. If you’re close to the 12-month mark, waiting even a few weeks to cross it could save you tens of thousands of dollars in taxes.

How can I reduce or defer capital gains tax on real estate?

Several strategies exist. A 1031 exchange defers both capital gains and depreciation recapture taxes by reinvesting proceeds into a like-kind property. The primary residence exclusion (Section 121) eliminates up to $250,000/$500,000 in gains if the property was your home for 2+ years. Opportunity Zone investments offer deferral and potential exclusion for qualifying gains. You can also increase your adjusted basis by documenting all capital improvements. Finally, harvesting losses on other investments can offset gains. Each strategy has specific rules — consult a tax professional before executing any of them.

What is the Net Investment Income Tax (NIIT)?

The NIIT is a 3.8% surcharge on net investment income — including capital gains from real estate — for taxpayers whose modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly). It applies on top of regular capital gains tax. On a $200,000 gain, the NIIT adds $7,600 to your tax bill. These thresholds haven’t changed since the tax was introduced in 2013, so inflation pushes more investors above the limit each year.

Are these calculations exact?

No. This the tax calculator provides estimates for planning purposes. Actual tax liability depends on your complete tax return, including other income, deductions, loss carryforwards, filing status, and state-specific rules. The calculator uses simplified assumptions — a flat state rate, upper-bound NIIT, and standard recapture at 25%. Always confirm your estimated tax with a CPA or tax attorney before closing on a sale.

Related Calculators

Complete your investment analysis with these tools

- 1031 Exchange Calculator — Model the tax deferral from a like-kind exchange. See how much you save by reinvesting proceeds versus selling outright.

- Real Estate ROI Calculator — Calculate total return on investment including appreciation, cash flow, equity buildup, and tax benefits. Compare holding vs. selling.

- Depreciation Calculator — Estimate annual and accumulated depreciation for residential and commercial rental property. Use this to fill in the depreciation input for this tool.

- NOI Calculator — Calculate Net Operating Income to evaluate whether holding the property generates better returns than selling and paying the tax.

- Cap Rate Calculator — Determine the capitalization rate of your current property or potential replacement properties in a 1031 exchange.

- Rental Property Calculator — Full rental analysis including cash flow, cash-on-cash return, and long-term wealth building. Model the “hold” scenario to compare against selling.

- BRRRR Calculator — If you’re selling one property to fund a BRRRR deal, compare the after-tax proceeds from the calculator against the capital needed for your next acquisition.

Disclaimer: This article is for educational purposes only and does not constitute financial, investment, legal, or tax advice. Real estate investing involves significant risk, including the potential loss of capital. All numbers, rates, and projections are illustrative examples and may not reflect your specific situation. Consult qualified financial, legal, and tax professionals before making any investment decisions.

Leave a Reply