In this article:

If you’re buying a rental property in 2026, one of the first decisions you’ll make is how to finance it — and the DSCR loan vs conventional debate is front and center for most investors. These two loan types approach qualification completely differently, carry different rates and costs, and fit different investor profiles. Choosing the wrong one can quietly kill your cash flow or shut you out of the deal entirely. This guide breaks down both products, compares them side by side, and gives you a clear framework for picking the right tool for your next deal.

What Is a DSCR Loan?

A DSCR loan is a non-QM mortgage designed for income-producing real estate. Instead of asking for W-2s, tax returns, or employment history, the lender evaluates whether the property generates enough rent to cover the mortgage payment.

DSCR = Gross Monthly Rent / Monthly PITIA

PITIA = Principal + Interest + Taxes + Insurance + Association dues. A DSCR of 1.0 means rent exactly covers the payment. Most lenders want 1.20+ for standard pricing. Use our DSCR calculator to run the ratio on any property.

How DSCR Qualification Works

- DSCR ratio: 1.20+ for best pricing, 1.0+ for standard approval

- Credit score: 660–680 minimum; better pricing at 720+

- Down payment: 20–25% SFR; 25–30% on 2–4 unit

- Reserves: 6–12 months PITIA post-closing

- No income docs: No W-2, no tax returns, no employment verification

DSCR Rates in 2026

DSCR rates run roughly 1.0–1.75% above conventional. With conventional investment rates at 7.0–7.5%, most DSCR borrowers see 7.75–8.5%. Shop at least three lenders — pricing varies significantly.

What Is a Conventional Mortgage for Investment Property?

A conventional mortgage conforms to Fannie Mae or Freddie Mac guidelines. For investment properties: higher down payment, higher rate, stricter reserves — but still meaningfully cheaper than DSCR.

Conventional Qualification

- Income verification: W-2s, tax returns (2 years), pay stubs

- DTI ratio: 36–45% max including all financed properties

- Credit score: 620 minimum, 740+ for best rate

- Down payment: 15% SFR investment, 25% on 2–4 unit

- Property count: Up to 10 financed properties (Fannie); lender overlays often cap lower

Conventional Rates in 2026

Investment property rate adjustments add 0.75–1.50% over primary residence rates. Expect 7.0–7.75% for a well-qualified borrower. Run numbers with our investment mortgage calculator.

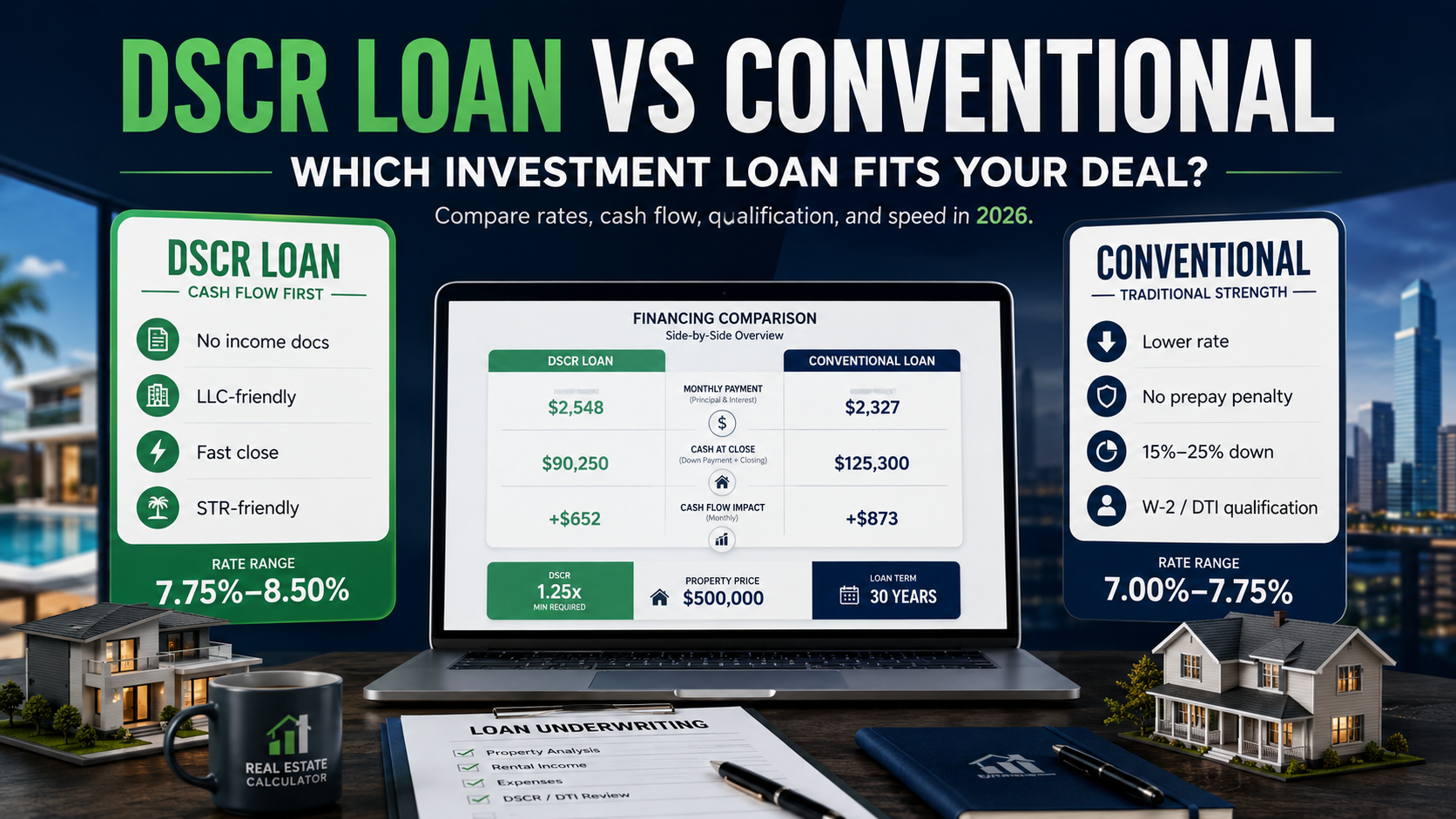

DSCR Loan vs Conventional: Side-by-Side

| Factor | DSCR Loan | Conventional |

|---|---|---|

| Qualification | Property cash flow | Borrower income + DTI |

| Income docs | None | W-2s, tax returns, pay stubs |

| Rate (2026) | 7.75% – 8.50% | 7.00% – 7.75% |

| Min down payment | 20–25% | 15–25% |

| LLC vesting | Yes | No (personal name only) |

| Property limit | Unlimited | 10 (Fannie Mae cap) |

| Closing speed | 14–21 days | 25–35 days |

| Prepayment penalty | Yes (3/2/1 typical) | None |

| STR eligible | Yes (many lenders) | Restricted |

When DSCR Loan Wins

Self-Employed with Heavy Write-Offs

If your taxable income shows $60K but actual cash flow is three times that, conventional lenders see a DTI problem. DSCR lenders never ask about your income.

Buying Inside an LLC

Conventional loans require personal name on title. DSCR lenders routinely close in LLC, LP, or trust — with just a personal guarantee.

5+ Financed Properties

Fannie Mae caps at 10; most lenders tighten at 4–6. DSCR lenders evaluate the new property in isolation — they don’t care how many you already own.

Need to Close Fast

DSCR: 14–21 days. Conventional: 25–35 days. In competitive markets, speed wins deals.

Short-Term Rentals

Conventional lenders want 12–24 months of lease history. New Airbnb? DSCR lenders accept STR income projections. Estimate potential with our Airbnb calculator.

When Conventional Mortgage Wins

You Qualify Easily and Want Lower Rate

The 0.75–1.25% rate advantage on a $300K loan = $150–$300/month extra cash flow. Over 5 years that’s $9,000–$18,000. Use our cash-on-cash calculator to see the impact.

First Investment Property

Clean qualifying picture? Start conventional — lowest rate, no prepayment penalty, builds your Fannie Mae track record.

House-Hacking (2–4 Unit Owner-Occupied)

FHA 3.5% down or conventional 5% down — massively lower entry cost than DSCR’s 20–25%. DSCR doesn’t apply to owner-occupied.

No Prepayment Penalty

Planning to refinance within 3 years? DSCR’s 3/2/1 penalty can cost $2,500–$7,500. Conventional has zero.

Real Cost Comparison: Same $300K Property

| Item | DSCR Loan | Conventional |

|---|---|---|

| Down payment | 25% / $75,000 | 20% / $60,000 |

| Loan amount | $225,000 | $240,000 |

| Rate | 8.25% | 7.25% |

| P&I payment | $1,690/mo | $1,638/mo |

| Total PITIA | $2,040/mo | $1,988/mo |

| Gross rent | $2,200/mo | $2,200/mo |

| DSCR ratio | 1.08 | 1.11 |

| Cash at close (est.) | ~$82,000 | ~$67,000 |

Neither produces positive cash flow after vacancy/maintenance at today’s rates — a 2026 reality check. DSCR requires $15K more upfront but skips income docs. Conventional is cheaper but consumes DTI capacity. Calculate your own scenario with our rental property calculator.

How Each Loan Affects DSCR Ratio and Cash Flow

DSCR loans carry higher rates, which means lower DSCR ratios on the same property. In the example above: DSCR loan = 1.08 ratio, conventional = 1.11. Both thin, but the DSCR loan is dangerously close to 1.0 if rents soften. Check your numbers with our DSCR calculator.

Over a 10-year hold, the 1% rate gap costs roughly $20,000–$25,000 more in total interest on DSCR. But if DSCR is the only loan that gets you approved, an imperfect loan on a good deal beats no deal. Model long-term returns with our rental ROI calculator.

Portfolio-level: every conventional loan increases your DTI. Around $500K–$800K in financed rental debt, most investors hit the DTI wall. DSCR loans don’t touch DTI at all — they’re the de facto scaling tool past 5–10 doors.

Common Mistakes When Choosing

Defaulting to DSCR because it’s easier. If you qualify conventionally, the rate savings often make conventional smarter. Don’t avoid gathering documents just because DSCR doesn’t require them.

Ignoring prepayment penalty. DSCR’s 3-year step-down penalty can cost 1–3% of loan balance. On $250K that’s $2,500–$7,500 if you sell/refi early.

Wrong rent figure for DSCR qualification. Lenders use the lesser of actual lease or appraiser’s market rent estimate. Above-market leases get haircut to appraised rent, dropping your DSCR.

Not modeling reserves. DSCR requires 6–12 months reserves post-closing. Model total cash-to-close with our closing costs calculator.

Not shopping DSCR rates. Non-QM pricing varies 0.5–1.0% across lenders for same profile. Always get 3+ quotes.

Decision Framework: Which Fits Your Profile?

Go Conventional If:

- W-2 or easy-to-document income

- DTI below 40% including new property

- Fewer than 4–6 financed properties

- Planning to hold 5+ years without early refi

- Buying as individual (not LLC)

- Rate minimization is top priority

Go DSCR If:

- Self-employed with write-offs compressing income

- Want to hold property in LLC

- 5+ financed properties, near conventional limit

- Need to close in under 21 days

- Buying a new STR with no lease history

- Scaling portfolio without impacting personal DTI

For macro rate context, the Federal Reserve’s H.15 release tracks benchmark rates influencing both loan types. The CFPB’s loan options guide explains QM vs non-QM distinctions.

Frequently Asked Questions

A conventional mortgage qualifies you based on personal income and DTI ratio. A DSCR loan qualifies the property based on whether rental income covers the mortgage payment — your personal income is not evaluated. This makes DSCR significantly more accessible for self-employed investors and those scaling a portfolio.

Yes, typically by 0.75–1.50 percentage points in 2026. DSCR loans are non-QM products without Fannie Mae backing, so lenders price in additional risk. However, rates vary widely across lenders — shopping aggressively can narrow the gap significantly.

Yes. DSCR lenders routinely close loans in LLC, LP, or trust with a personal guarantee. Conventional mortgages require personal name on title and cannot close in an entity. If LLC ownership is part of your strategy, DSCR is typically the only institutional option.

Most lenders require minimum 1.0 (rent equals PITIA), with better pricing at 1.20+. Some go down to 0.75 with higher down payment or rate premium. A ratio of 1.25+ unlocks the best rates and LTV options.

Fannie Mae allows up to 10 financed properties, but most lenders apply overlays capping at 4–6. Reserve requirements increase substantially with each property. Once you approach that ceiling, DSCR and portfolio loans become the primary scaling tools.

Yes, nearly all DSCR loans carry prepayment penalties — typically 3/2/1 step-down (3% year one, 2% year two, 1% year three). Selling or refinancing during this window triggers the penalty. Conventional mortgages have zero prepayment penalties.

Disclaimer: This article is for educational purposes only and does not constitute financial, legal, or mortgage advice. Loan rates, guidelines, and qualifying criteria change frequently and vary by lender. All figures reflect general 2026 market conditions and are not guaranteed. Consult a licensed mortgage professional before making lending decisions.

Leave a Reply