In this article:

- Before You Run Any Numbers

- Step 1: Screen With the 70% Rule or Rent-to-Price

- Step 2: Estimate After-Repair Value

- Step 3: Build a Rehab Budget

- Step 4: Calculate NOI and Cash Flow

- Step 5: Check DSCR and Financing

- Step 6: Model Total ROI Over Time

- Step 7: Compare Strategies

- Where First-Time Investors Blow It

- FAQ

Learning how to analyze real estate deal opportunities is the single most important skill for a new investor. Your first deal will feel overwhelming — too many numbers, too many opinions, and too many ways to get it wrong. I know because my first deal lost money. Not because the property was bad, but because I skipped steps in the analysis and made assumptions I should have verified.

This walkthrough shows you how to analyze real estate deal numbers through the exact sequence of calculators and checks that experienced investors use to analyze a deal. Not theory. The actual steps, in order, with the tools that make each step faster.

Before You Run Any Numbers

Two things matter before you analyze real estate deal details or open a single calculator.

Know your strategy. Are you buying a rental to hold for 10 years? Flipping for quick profit? Running a BRRRR? Each strategy uses different calculators and different success metrics. A deal that fails as a flip might work perfectly as a rental. Decide what you are doing before you start analyzing.

Know your market. Drive the neighborhoods. Check days on market for rentals. Talk to a property manager about realistic rents. Look at recent sales. The best calculator in the world cannot fix bad inputs, and bad inputs almost always come from not knowing the local market.

Step 1: Analyze Real Estate Deal Basics — Quick Screen

Most properties fail the first filter. Save yourself time by screening fast before doing deep analysis.

For flips: Use the 70% rule calculator. Enter ARV and estimated rehab. If the maximum allowable offer is below the asking price, move on. You can adjust the percentage for your market, but 70% is a solid starting screen.

For rentals: Check the rent-to-price ratio. Monthly rent divided by purchase price. Below 0.7% at current rates means the deal is almost certainly cash-flow negative with financing. Above 0.8% is worth deeper analysis. The rental property calculator runs this in seconds.

I screen about 30 properties for every one I analyze in depth. This step eliminates 80% of listings in under a minute each.

Step 2: Estimate After-Repair Value

ARV is the foundation. Every other number depends on it. Get this wrong and everything downstream is fiction.

The ARV calculator helps you build a value estimate from comparable sales. Pull 3-5 recent sales of similar renovated properties within a half-mile radius. Adjust for size, condition, and lot differences.

Common mistake here: using Zillow Zestimate as your ARV. Zestimates are automated and often wrong for distressed or recently renovated properties. Use actual closed sales from the MLS or county records.

Another mistake: using the highest comp as your ARV. Use the median. If your five comps are $210K, $225K, $230K, $245K, and $280K, your ARV is around $230K. Not $280K.

Step 3: Build a Real Rehab Budget

If the property needs work, your rehab budget is the second most important number after ARV.

The rehab cost estimator breaks renovation into categories: kitchen, bathrooms, flooring, paint, systems, structural, exterior. This prevents the single biggest mistake beginners make — guessing a lump sum without breaking down scope.

Get contractor bids for major items. Add 15-20% contingency for hidden conditions. Include soft costs: permits, dumpsters, temporary utilities. On a typical moderate rehab, soft costs add $4,000-8,000 that most beginners forget entirely.

For hard money financed flips, your rehab budget also affects your loan amount and interest costs. The hard money loan calculator shows how points, interest rate, and draw schedule change your total financing cost.

Step 4: Calculate NOI and Cash Flow

For rental properties, this is where the deal lives or dies.

Calculate Net Operating Income First

Start with the NOI calculator. Enter gross rent, vacancy (use 7-8%, never zero), and operating expenses broken out by category: property tax, insurance, management, maintenance, CapEx reserves, utilities, HOA.

NOI tells you what the property earns before debt service. It is the number that drives cap rate, DSCR, and property valuation.

This is the money that actually lands in your account each month. If it is negative, you are subsidizing your tenant’s housing.

Check the vacancy rate calculator separately. A 3-percentage-point change in vacancy assumption can flip a deal from positive to negative. Know what vacancy actually looks like in your submarket.

Step 5: Check DSCR and Financing

If you are financing the purchase and need to check financing, the lender cares about one number more than any other: DSCR. Debt Service Coverage Ratio is NOI divided by annual debt service. Below 1.0 means the property does not cover its mortgage from income. Most lenders want 1.20 or higher.

Compare Loan Options and Returns

The investment property mortgage calculator shows your full PITI (principal, interest, taxes, insurance) and how it compares against rental income. This is also where you check whether your loan-to-value ratio works for the loan program you plan to use.

Run the cash-on-cash calculator to see your Year 1 return on actual cash invested. This metric answers: “What is my money earning sitting in this deal versus sitting in the stock market?”

For reference, the cap rate calculator strips out financing and shows the property’s income yield. Useful for comparing properties regardless of how you finance them.

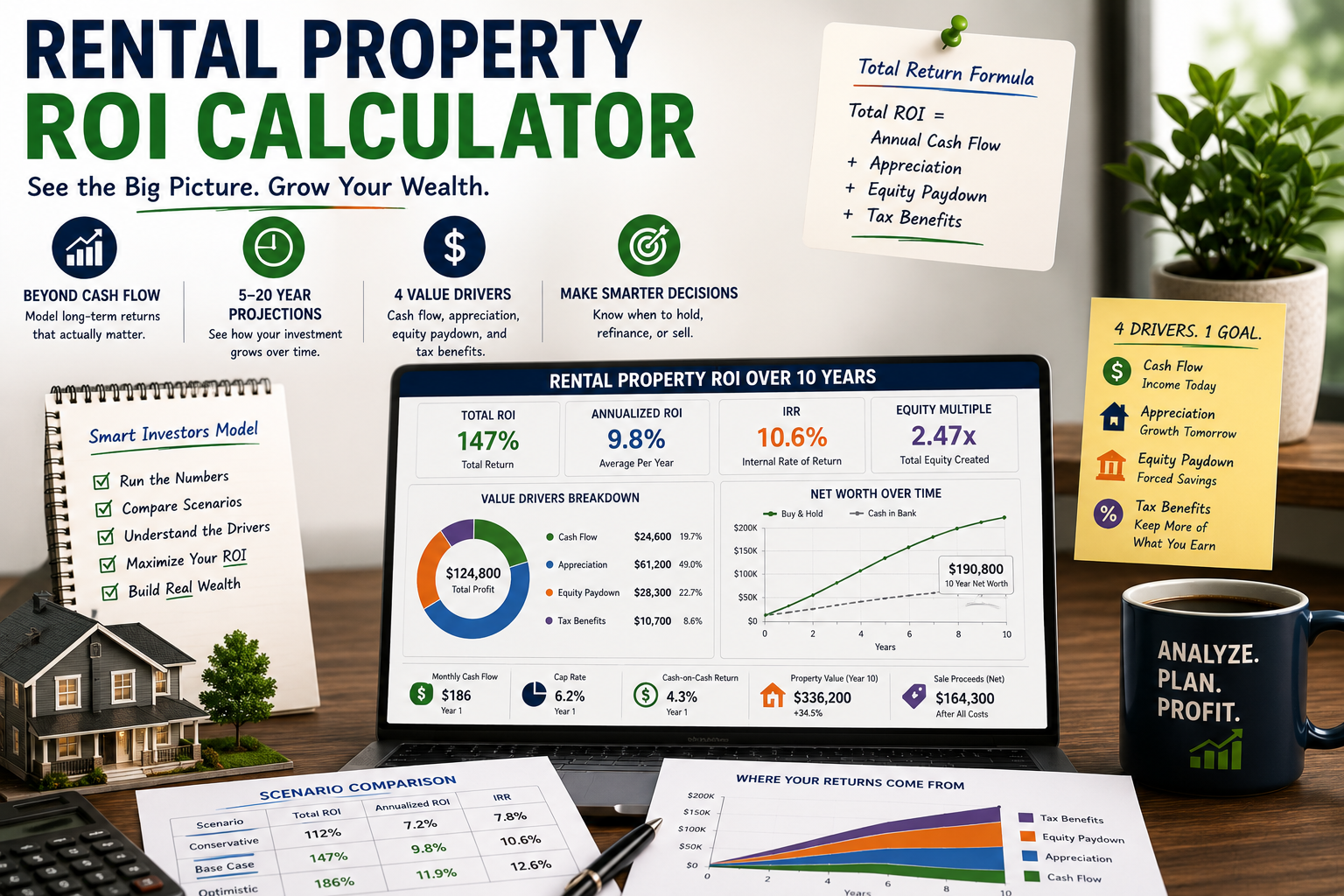

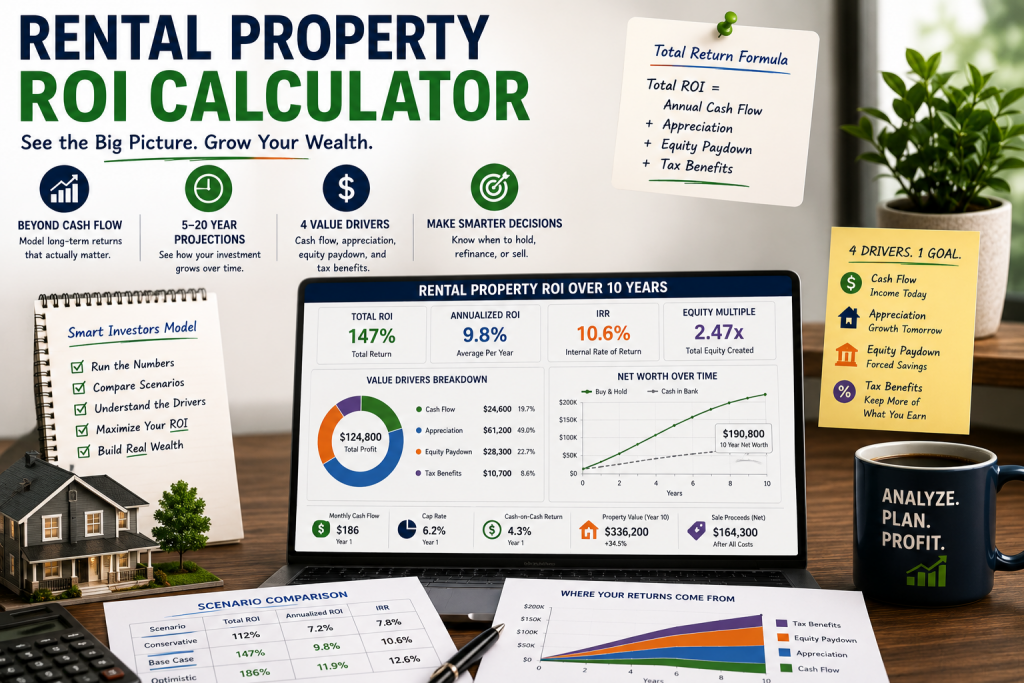

Step 6: Model Total ROI Over Time

Year 1 metrics only tell part of the story. Rental wealth builds through cash flow, appreciation, equity paydown, and tax effects compounding over years.

Project Long-Term Wealth Building

The rental property ROI calculator models a 5-20 year hold and shows total return including all four value drivers. A deal with mediocre Year 1 cash flow can produce strong total ROI over a 10-year hold if appreciation and equity paydown do the work.

For time-value analysis, the IRR calculator shows annualized return accounting for when cash flows happen. IRR is how professional investors compare deals with different timelines.

The real estate ROI calculator compares rental, flip, and BRRRR strategies side by side using the same property assumptions. Helpful when you are not sure which strategy fits a particular deal.

Step 7: Compare and Decide

When looking at multiple properties, the compare deals calculator puts them side by side. Same metrics, same assumptions, clear winner.

Strategy-Specific Tools

For flips specifically, the fix and flip calculator and house flipping profit calculator model the full project from purchase through sale, including financing costs, holding costs, and selling costs.

For BRRRR, the BRRRR calculator models buy-rehab-rent-refinance and shows how much capital you recover through the refi. The BRRRR refinance calculator focuses specifically on the refi step.

If you are deciding between renting and buying a primary residence, that is a completely different analysis. The rent vs buy calculator handles that comparison.

And before you sell any property, run the numbers through the capital gains tax calculator and 1031 exchange calculator to understand the tax impact.

Common Mistakes When You Analyze Real Estate Deal Numbers

Looking at only one property and buying it. Analyze 20-30 before making your first offer. You need pattern recognition that only comes from running lots of deals through the numbers.

Using optimistic assumptions. Agents show you best-case numbers. Sellers show you pro forma income. Use conservative vacancy (7-8%), real expense ratios (40-50%), and verified rent comps. If the deal only works with optimistic inputs, it does not work.

Skipping the inspection. A $400 inspection can reveal $15,000-30,000 in hidden problems. Foundation, roof, HVAC, plumbing, electrical. Everything you do not find before buying becomes your expensive surprise after closing.

Not having reserves. Budget 6 months of mortgage payments plus $5,000-10,000 for unexpected repairs in a separate account. Properties eat cash in the first year, and running out of reserves is how investors lose properties.

Analysis paralysis. At some point you have to stop calculating and make an offer. The deal does not need to be perfect. It needs to make sense with conservative assumptions and reasonable reserves. Done beats perfect in real estate investing.

Your Deal Analysis Checklist to Analyze Real Estate Deal Opportunities

Before you make an offer, confirm every item on this checklist. Each step helps you analyze real estate deal numbers with confidence rather than guesswork.

Pre-Offer Verification Steps

- Market rent verification. Confirm rental rates with at least three sources: Rentometer, Zillow rental listings, and a local property manager. Never rely on the seller’s stated income.

- Expense audit. Call the insurance company for an actual quote. Pull property tax records from the county assessor. Get a management fee quote even if you plan to self-manage — your time has value.

- Financing pre-approval. Know your rate, terms, and down payment requirement before running calculators. The difference between 7.0% and 7.5% interest changes monthly cash flow by $30-50 per $100K financed.

- Exit strategy clarity. Know how you will exit this deal before you enter it. Buy-and-hold needs strong cash flow. Flips need margin. BRRRR needs ARV high enough to refinance out your capital.

- Reserve confirmation. Have 6 months of PITI plus a $5,000-10,000 repair fund in a separate account before closing. Do not count on rental income to cover emergencies from day one.

When to Walk Away

Walk away when the deal only works with optimistic assumptions. If you need 3% vacancy, above-market rents, or zero maintenance to make the numbers positive, the deal does not work. Walk away when the inspection reveals structural, foundation, or major system issues that were not priced into your rehab budget. Walk away when comparable sales do not support the ARV you need. These are not failures — they are the analysis doing its job. Most properties should not become investments, and recognizing that quickly is what separates successful investors from those who lose money on their first deal.

Use the gross rent multiplier calculator as a final sanity check. GRM gives you a quick ratio of price to gross rent that you can compare across markets and property types. Combined with the property management fee calculator, you will have a complete picture of what this property costs to own and operate.

Every experienced investor will tell you the same thing: the deal you analyze and reject teaches you as much as the one you buy. Build your analysis muscle by running 30 properties through this system. By the time you find the right deal, you will know it immediately.

Frequently Asked Questions

It depends on your strategy. For rentals, cash flow after all expenses and debt service matters most for daily operations, while total ROI matters for wealth building. For flips, net profit after all costs determines success. For BRRRR, capital recovery through refinance is the key metric. No single number tells the whole story, which is why you should look at metrics from multiple angles.

At least 20-30. Running numbers on many properties builds intuition for what good deals look like in your market. Most properties fail the first screening step, so analyzing 30 might only take a few hours total once you have a system.

Start with a quick screen. For flips, use the 70% rule calculator. For rentals, use the rental property calculator with rent-to-price ratio. These filter out non-starters so you only spend time on deals in under a minute so you only spend time on deals that might actually work.

No. Even in strong markets, tenant turnover happens. Use 5-8% vacancy as a planning assumption. If the deal only works at 0% vacancy, it does not work. One month of vacancy per year is roughly 8% and is realistic for most single-family and small multifamily rentals.

35-50% of effective gross income for single-family rentals. 45-55% for small multifamily. These include property tax, insurance, vacancy, maintenance, management, CapEx reserves, and administrative costs. If your total expenses are under 30%, you are probably missing line items.

For a conventional investment property loan: 25% down payment plus 3-5% closing costs plus rehab budget plus 6 months reserves. On a $200,000 property with no rehab needed, plan for roughly $65,000-75,000 total. FHA loans on 2-4 unit properties where you live in one unit can reduce the down payment to 3.5%.

Disclaimer: This article is for educational planning purposes only. All calculators mentioned provide estimates based on user-entered assumptions. Real estate investing involves risk including potential loss of capital. Verify all assumptions with local market data, professional inspections, lender quotes, and qualified advisors before making investment decisions. Market data from the National Association of Realtors and Census Bureau may provide useful regional context.

Leave a Reply