What Is a BRRRR Refinance?

A BRRRR refinance calculator helps investors model whether the refinance step will return their capital. Before committing to a deal, running the numbers through a calculator reveals exactly how much cash stays in — or comes back out.

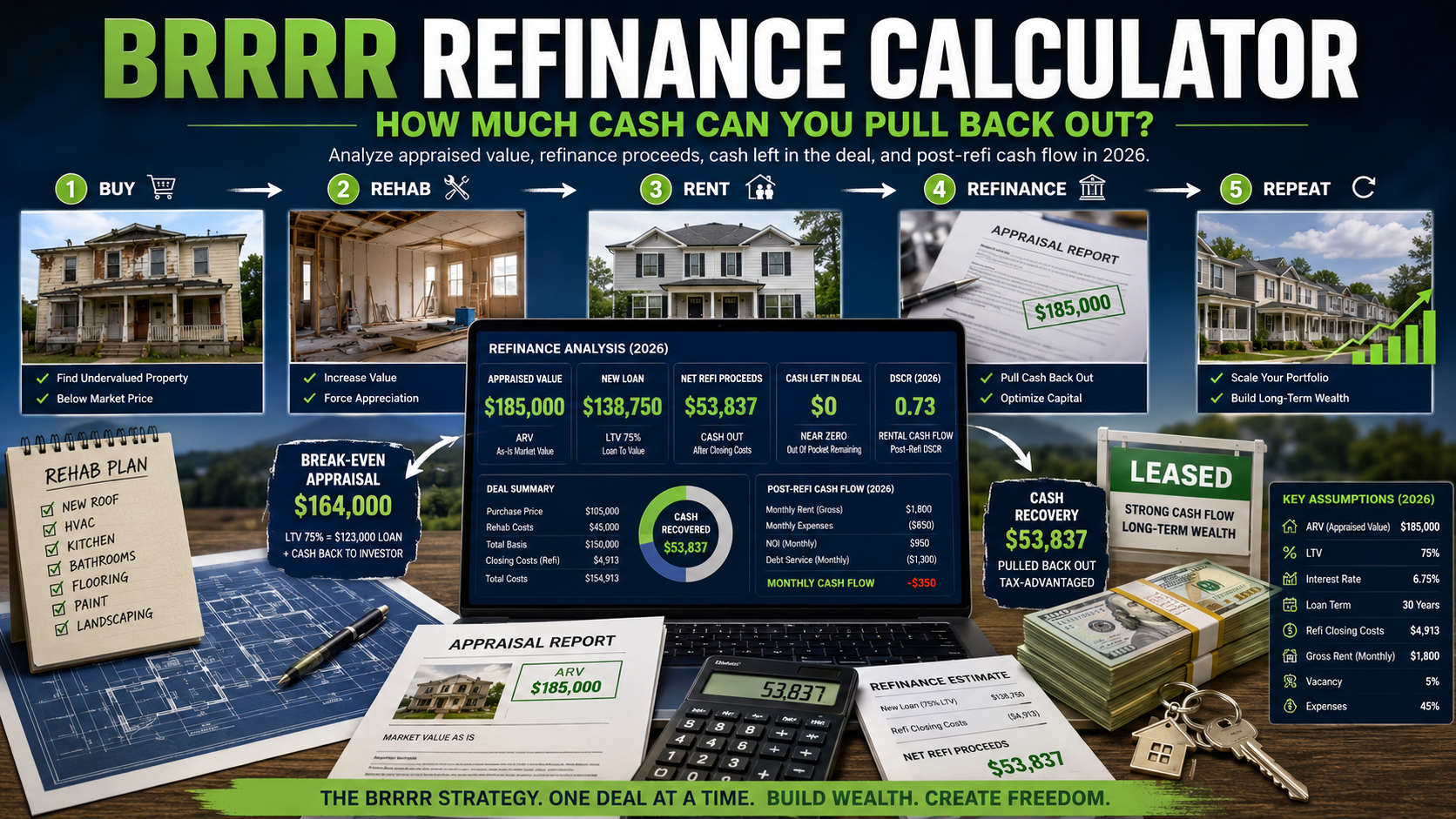

A BRRRR refinance is the fourth step of the Buy, Rehab, Rent, Refinance, Repeat strategy. After purchasing a distressed property, renovating it, and placing a tenant, the investor refinances the property based on its new, higher appraised value. The goal is to pull out most or all of the original cash invested so it can be recycled into the next deal.

The refinance is the make-or-break moment in any BRRRR deal. If the appraised value comes in high enough and the loan terms are favorable, the investor recovers their capital and keeps a cash-flowing rental. If the appraisal falls short or the numbers are tight, money stays trapped in the deal — and the “Repeat” part of the strategy stalls.

This guide walks through how to calculate your BRRRR refinance proceeds, what drives success or failure at the refinance stage, and how to stress-test your deal before you commit. Use our free BRRRR Refinance Calculator to run the numbers on any property.

How the BRRRR Refinance Works Step by Step

The refinance step connects everything in the BRRRR chain. Here is what happens in practice:

- Complete the rehab and stabilize the rental. Most lenders require the property to be tenant-occupied and seasoned for 3 to 12 months before they will refinance.

- Order an appraisal. The lender sends an appraiser who determines the current market value of the renovated property. This number controls how much you can borrow.

- Apply for a cash-out refinance loan. Common options include conventional loans (up to 75% LTV for investment properties), DSCR loans (up to 80% LTV with no income verification), and portfolio loans from local banks.

- Receive loan proceeds and pay off existing debt. The new loan pays off the original purchase financing (hard money loan, private money, or HELOC). Any remaining proceeds go back to the investor as recovered cash.

- Calculate cash left in the deal. This is the difference between your total investment (purchase + rehab + closing costs + holding costs) and the net refinance proceeds. A successful BRRRR leaves zero or near-zero cash in the deal.

BRRRR Refinance Formula

Every BRRRR refinance calculator uses the same core formula:

| Variable | Formula |

|---|---|

| Max Loan Amount | Appraised Value × LTV Ratio |

| Net Refi Proceeds | Max Loan Amount − Payoff Balance − Refinance Closing Costs |

| Cash Left in Deal | Total Cash Invested − Net Refi Proceeds |

| Cash-on-Cash Return | Annual Cash Flow ÷ Cash Left in Deal |

When Cash Left in Deal equals zero, the investor has achieved an “infinite return” — all original capital has been recovered while the rental property continues generating income.

Worked Example: Cleveland Duplex

Sarah buys a duplex in Cleveland for $95,000 using a hard money loan at 85% LTV ($80,750 loan, $14,250 down payment). She spends $35,000 on rehab and $4,200 on holding costs during the 4-month renovation. Her total cash invested is $53,450 ($14,250 down + $35,000 rehab + $4,200 holding).

After placing tenants at $1,400/month combined rent, she refinances at 6 months. The property appraises at $185,000. She gets a DSCR loan at 75% LTV.

| Item | Amount |

|---|---|

| Appraised Value | $185,000 |

| New Loan (75% LTV) | $138,750 |

| Hard Money Payoff | $80,750 |

| Refi Closing Costs (3%) | $4,163 |

| Net Refi Proceeds | $53,837 |

| Total Cash Invested | $53,450 |

| Cash Left in Deal | −$387 (all cash recovered + $387 profit) |

Sarah recovered all her cash and has $387 extra. She now owns a rental property producing $1,400/month in rent with $0 of her own money tied up. Her next step: repeat the process with a second property.

What Drives Refinance Success

Three variables determine whether a BRRRR refinance works:

1. The Spread Between Purchase Price and After-Repair Value

The bigger the gap between what you paid (plus rehab) and what the property appraises for, the more equity you create. Most successful BRRRR investors target properties where total cost (purchase + rehab) is 65% to 75% of the expected after-repair value.

If your all-in cost exceeds 75% of ARV and the lender caps LTV at 75%, you will leave cash in the deal by definition. This is simple math, and it is the single most common reason BRRRR deals underperform.

2. The Appraised Value

You can estimate ARV all day, but the number that matters is what the lender’s appraiser puts on paper. Appraisals follow USPAP standards and are based on comparable sales within the past 6 to 12 months. In neighborhoods with few recent sales or volatile pricing, appraisals can come in below your estimate.

Protect yourself by pulling 5 to 8 comparable sales before making an offer. Focus on properties with similar square footage, bedroom count, and condition within a half-mile radius. If you cannot find solid comps, the deal carries appraisal risk.

3. Loan Terms (LTV and Rate)

Higher LTV means more cash back. A 75% LTV refinance on a $200,000 appraisal produces $150,000. At 80% LTV, that jumps to $160,000 — an extra $10,000 of recovered capital. DSCR lenders often go to 80% LTV, while conventional investment property loans typically cap at 75%.

Interest rate matters less at the refinance stage (it affects monthly cash flow, not cash recovery) but becomes critical for long-term hold analysis. Use the DSCR Calculator to check whether your post-refinance payment fits the rental income.

Why BRRRR Refinances Fail

Understanding failure modes helps you avoid them:

Rehab budget overruns. Every dollar over budget is a dollar that stays in the deal. A $35,000 rehab that balloons to $50,000 adds $15,000 to your cash-left-in-deal. Get three contractor bids, add a 15% contingency, and use the Rehab Cost Estimator to benchmark your numbers.

Low appraisal. If the property appraises for $160,000 instead of $185,000, your max loan drops from $138,750 to $120,000 at 75% LTV. That is $18,750 less cash returned. You can challenge the appraisal with better comps, request a second appraisal, or wait 6 months for the market to catch up — but none of these are guaranteed.

Seasoning requirements. Most lenders require 3 to 12 months between purchase and refinance. If you planned to refinance at 3 months but your lender requires 6, you carry extra holding costs (mortgage payments, insurance, property taxes) that eat into your return.

Rent shortfall. DSCR lenders require the property’s rental income to cover debt service, typically at a 1.0 to 1.25 ratio. If market rents are lower than expected, you either get a smaller loan, pay a higher rate, or get denied entirely.

Over-improving the property. Installing granite countertops and hardwood floors in a $120,000 neighborhood does not add proportional value. Match your rehab scope to the neighborhood price ceiling. The ARV Calculator helps you validate your after-repair value against local comps.

Cash Left in Deal vs. Cash Recovered

These are the two numbers that define BRRRR success:

| Outcome | What It Means | How Common |

|---|---|---|

| Cash Left = $0 | All capital recovered. “Infinite return” achieved. | Rare — requires strong execution and a cooperative appraisal |

| Cash Left = $5,000–$15,000 | Most capital recovered. Still a good deal if cash flow is strong. | Common in competitive markets |

| Cash Left = $20,000+ | Significant capital trapped. Slows your ability to repeat. | Often signals overpaying or over-rehabbing |

| Cash Left < $0 (negative) | You pulled out more than you invested. Excess cash in pocket. | Happens when ARV significantly exceeds total cost |

A common mistake is focusing only on whether you get all your cash back. A deal that leaves $8,000 in but produces $500/month in cash flow is better than a deal that returns all capital but only generates $100/month. Always evaluate the refinance alongside cash flow and cash-on-cash return.

Post-Refinance DSCR: Will the Property Cash Flow?

After refinancing, your monthly payment increases because the new loan is typically larger than the original purchase financing. The critical question: does the rental income still cover the new payment?

DSCR (Debt Service Coverage Ratio) measures this:

DSCR = Net Operating Income ÷ Annual Debt Service

A DSCR above 1.25 means the property generates 25% more income than needed to cover the mortgage. Below 1.0 means you are subsidizing the property out of pocket every month.

Using Sarah’s Cleveland duplex example:

| Item | Monthly | Annual |

|---|---|---|

| Gross Rent | $1,400 | $16,800 |

| Vacancy (7%) | −$98 | −$1,176 |

| Property Tax | −$231 | −$2,775 |

| Insurance | −$108 | −$1,300 |

| Maintenance (8%) | −$112 | −$1,344 |

| Property Management (10%) | −$140 | −$1,680 |

| NOI | $711 | $8,525 |

| Mortgage Payment ($138,750 @ 7.5%, 30yr) | −$970 | −$11,641 |

| Cash Flow | −$259 | −$3,116 |

| DSCR | 0.73 | |

Despite getting all her cash back, Sarah’s duplex has negative cash flow after refinancing. The DSCR of 0.73 means she pays $259/month out of pocket. This is a real risk in the BRRRR strategy — recovering capital is not the same as owning a profitable rental.

To avoid this, run both the BRRRR Refinance Calculator and the DSCR Calculator before making an offer. If the post-refinance DSCR is below 1.0, either negotiate a lower purchase price, reduce rehab scope, or target higher-rent properties.

Break-Even Appraised Value

This is the minimum appraisal needed to recover all your cash. The formula:

Break-Even Appraised Value = (Total Cash Invested + Payoff Balance + Refi Closing Costs) ÷ LTV Ratio

For Sarah’s deal: ($53,450 + $80,750 + $4,163) ÷ 0.75 = $184,484. Her actual appraisal of $185,000 barely cleared the break-even threshold by $516.

Use the BRRRR refinance calculator to find your break-even appraisal before making an offer. If it requires the property to appraise above realistic comparable sales, the BRRRR math does not work for that deal.

Refinance Loan Options Compared

| Loan Type | Max LTV | Typical Rate | Seasoning | Best For |

|---|---|---|---|---|

| Conventional (Fannie/Freddie) | 75% | 6.5%–7.5% | 6–12 months | Lowest rate, investors with W-2 income |

| DSCR Loan | 75%–80% | 7.0%–8.5% | 3–6 months | No income docs, faster seasoning |

| Portfolio / Community Bank | 70%–80% | 7.0%–8.0% | Negotiable | Flexible terms, relationship-based |

| Commercial (5+ units) | 70%–75% | 7.0%–8.5% | 3–6 months | Multifamily BRRRR deals |

DSCR loans have become the most popular refinance vehicle for BRRRR investors because they qualify based on property income rather than personal income, and seasoning periods are shorter. See our DSCR Loans Guide for a detailed breakdown of lender requirements. For a step-by-step deal screening process, see how to screen rental property deals.

Sensitivity Analysis: How Appraisal Affects Your Return

The BRRRR refinance calculator sensitivity table shows how small changes in appraised value have a major impact on cash recovery. Using Sarah’s deal as a baseline:

| Appraised Value | New Loan (75% LTV) | Net Proceeds | Cash Left in Deal |

|---|---|---|---|

| $165,000 | $123,750 | $38,838 | $14,612 |

| $175,000 | $131,250 | $46,338 | $7,112 |

| $185,000 | $138,750 | $53,837 | −$387 |

| $195,000 | $146,250 | $61,337 | −$7,887 |

| $205,000 | $153,750 | $68,837 | −$15,387 |

A $10,000 drop in appraisal costs $7,500 in recovered cash at 75% LTV. Run multiple scenarios through the BRRRR refinance calculator before making an offer. Conservative ARV estimates are essential — optimistic projections lead to nasty surprises at the refinance stage.

Common Mistakes to Avoid

Ignoring closing costs on both ends. BRRRR investors pay closing costs twice — once when buying, once when refinancing. Budget 2% to 4% of the loan amount for each transaction. On a $140,000 refinance loan, that is $4,200 to $5,600 that comes directly out of your cash recovery.

Using short-term rental income for DSCR qualification. Most DSCR lenders use long-term rental comps, not actual income. If you plan to Airbnb the property, confirm the lender accepts STR income (many do not). Use the Airbnb Calculator to estimate nightly rates, but run DSCR with long-term rents as a conservative baseline. Learn more about how much you can make on Airbnb vs long-term rental.

Forgetting holding costs. Every month between purchase and refinance costs money: mortgage interest on the hard money loan, property taxes, insurance, utilities, lawn care. A 6-month hold at $1,800/month adds $10,800 to your total investment.

Not accounting for capital expenditures. Even after rehab, roofs age, HVAC units break, and water heaters fail. Budget 5% to 10% of gross rent for future capital expenditures when projecting long-term cash flow. The IRS Publication 527 covers depreciation and expense rules for rental property owners.

When BRRRR Refinance Does Not Make Sense

Even with a strong BRRRR refinance calculator result, the strategy is not right for every deal or every investor:

- Tight markets with small value-add spreads. If properties sell near their renovated value, there is no equity to create. A standard buy-and-hold with 20% to 25% down may be simpler and less risky.

- Rising interest rates. Higher refinance rates reduce cash flow and can push DSCR below lender minimums. A deal that worked at 6% rates may not work at 8%.

- Properties in declining neighborhoods. If comparable values are falling, your appraisal may come in lower 6 months from now than it would today. BRRRR works best in stable or appreciating areas.

- Investors who need immediate cash flow. The months between purchase and refinance produce little or no cash flow (you are paying hard money interest and funding rehab). If you need income now, a turnkey rental is a better fit.

How to Use the BRRRR Refinance Calculator

Our free BRRRR Refinance Calculator walks you through the full refinance analysis in three modes:

- Standard Mode: Enter purchase price, rehab cost, holding costs, appraised value, LTV ratio, and refinance rate. The calculator returns net proceeds, cash left in deal, post-refi DSCR, monthly cash flow, and break-even appraised value.

- Reverse Solve — Target Cash Left: Enter your target cash-left-in-deal (for example, $0 for full recovery) and the calculator tells you the minimum appraised value needed.

- Reverse Solve — Target DSCR: Enter your minimum acceptable DSCR (for example, 1.25) and the calculator determines the maximum loan amount and corresponding LTV.

Each mode includes a sensitivity table showing how results change across a range of appraised values and interest rates.

Disclaimer

This article and the associated calculator are for educational purposes only. Results are estimates based on user-entered assumptions and do not constitute financial, investment, tax, legal, or lending advice. Actual refinance terms, appraised values, closing costs, and rental income may differ from estimates. Consult a licensed mortgage professional, real estate attorney, and tax advisor before making investment decisions. ArvCalc is not a lender, broker, or financial advisor.

Seasoning requirements vary by lender. DSCR lenders typically require 3 to 6 months from the date of purchase. Conventional lenders (Fannie Mae, Freddie Mac) require 6 to 12 months. Some portfolio lenders and credit unions have no seasoning requirement at all. The shorter the seasoning period, the faster you recover your capital and can move to the next deal.

Most lenders offer 70% to 80% LTV on investment property cash-out refinances. Conventional loans typically cap at 75% LTV. DSCR loans may go up to 80% LTV if the property has strong rental income and a DSCR above 1.25. Higher LTV means more cash returned but also a larger monthly payment and lower cash flow.

A low appraisal reduces the maximum loan amount, which means less cash recovered. Your options include: challenging the appraisal by providing better comparable sales to the lender, requesting a second appraisal (some lenders allow this for a fee), waiting several months and trying again if the market is appreciating, or accepting a smaller refinance and leaving more cash in the deal.

Yes. DSCR loans are among the most popular refinance products for BRRRR investors. They qualify based on the property’s rental income relative to the mortgage payment rather than the borrower’s personal income. This makes them accessible to self-employed investors and those who own multiple properties. Minimum DSCR requirements typically range from 1.0 to 1.25 depending on the lender.

Yes. If the appraised value is significantly higher than your total investment, the refinance proceeds can exceed your cash outlay. This results in negative “cash left in deal,” meaning you receive excess cash at closing. This is most common in deals where the investor bought well below market value or the local market appreciated during the rehab and seasoning period.

If you recover all your cash (cash left in deal equals zero), cash-on-cash return is technically infinite because the denominator is zero. For deals where some cash stays in, most BRRRR investors target 12% or higher cash-on-cash return. Below 8% generally suggests the deal is underperforming relative to the effort and risk involved.

Divide your total investment (purchase down payment + rehab costs + holding costs + all closing costs) plus the existing loan payoff amount by your refinance LTV ratio. The result is the minimum appraised value needed to recover all your cash. For example, if your total cash invested is $50,000, loan payoff is $80,000, refi closing costs are $4,000, and LTV is 75%, the break-even appraisal is ($50,000 + $80,000 + $4,000) ÷ 0.75 = $178,667.

Leave a Reply