Why You Need a Real Estate Deal Analysis Checklist

Every bad real estate deal started with skipped steps. The investor ran one metric, trusted the seller’s numbers, or fell in love with the property before doing the math. A real estate deal analysis checklist prevents these costly mistakes by forcing you through every critical check before writing a contract.

This checklist covers the 10 steps experienced investors follow on every deal — from initial screening to final underwriting. Each step includes what to check, what numbers to run, and what kills the deal. Use it alongside our free Rental Property Calculator and the complete deal analysis guide.

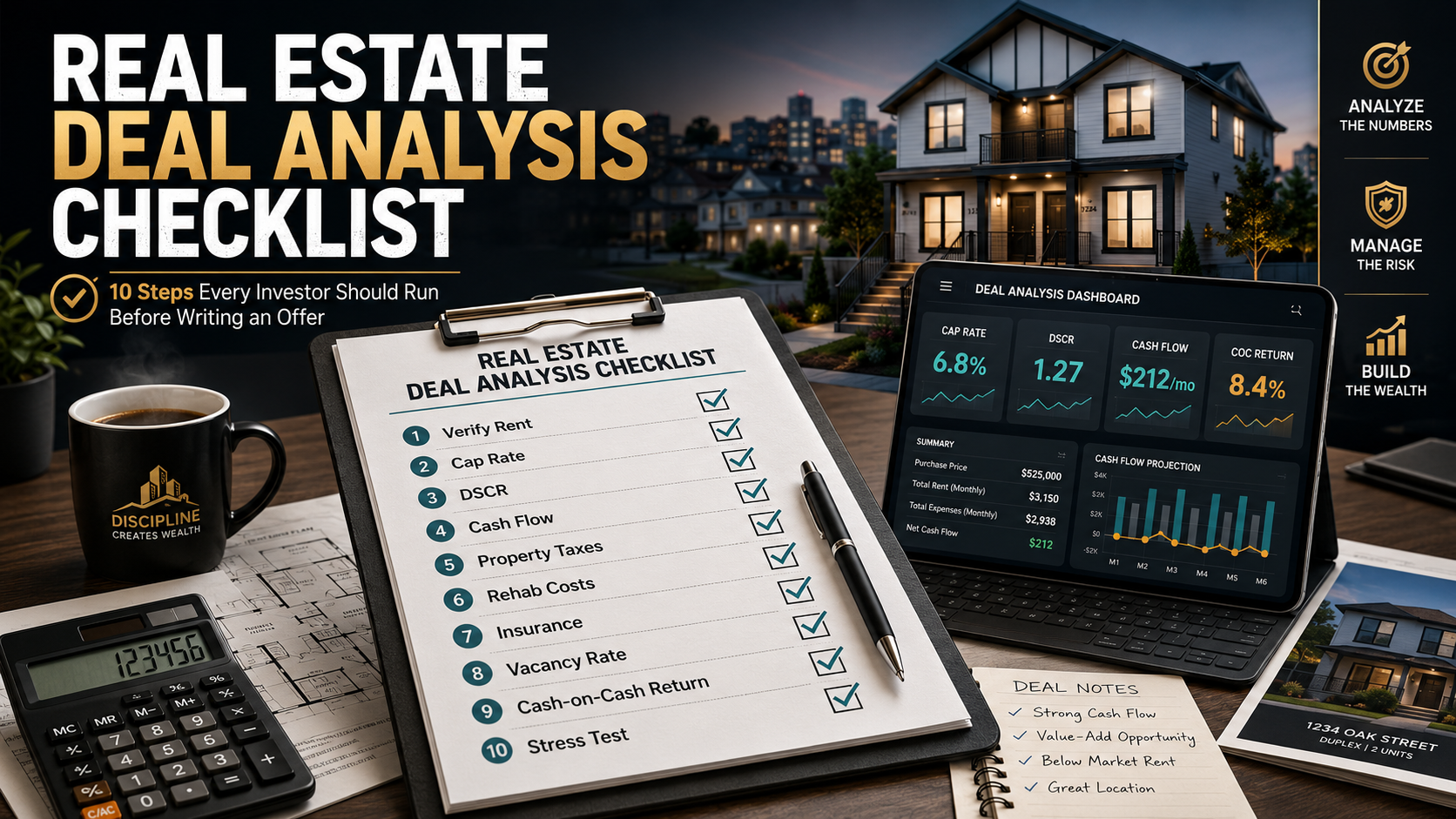

The 10-Step Real Estate Deal Analysis Checklist

Print this real estate deal analysis checklist or bookmark it. Run every step on every deal — no exceptions.

Step 1: Verify the Rent

Never trust the seller’s rent number. Verify with three sources:

- Check 3-5 active comparable listings on Zillow, Apartments.com, or Craigslist within a half-mile radius

- Pull HUD Fair Market Rent for the zip code as a floor

- If the property has tenants, request 12 months of bank statements or lease agreements

Kill signal: Seller claims rent is 20%+ above comparable listings. They are inflating income to justify the price.

Step 2: Calculate Cap Rate

Cap rate tells you if the price is reasonable for the income the property produces.

Formula: Cap Rate = NOI ÷ Purchase Price × 100

Quick version: (Monthly Rent × 12 × 0.60) ÷ Price. The 0.60 assumes 40% operating expenses.

| Cap Rate | Action |

|---|---|

| 7%+ | Strong — proceed to step 3 |

| 5%–7% | Okay in stable markets — check other metrics carefully |

| Below 5% | Only works for appreciation plays — skip for cash flow |

Run it: Cap Rate Calculator

Step 3: Run DSCR

DSCR tells you whether the property covers its own mortgage payment. If you plan to finance the deal, this is your go/no-go gate.

Formula: DSCR = Gross Rent ÷ PITIA

| DSCR | Action |

|---|---|

| 1.25+ | Strong — best loan pricing |

| 1.0–1.25 | Passes — but thin margin |

| Below 1.0 | Kill the deal or renegotiate price |

Run it: DSCR Calculator. For DSCR loan specifics, see the DSCR Loans Guide.

Step 4: Calculate Cash Flow

This is the number that determines whether the property puts money in your pocket or costs you money every month. Include every expense — not just the mortgage.

Cash Flow = Gross Rent − Vacancy − Taxes − Insurance − Maintenance − CapEx − Management − Mortgage

Minimum target: $100/month per unit for buy-and-hold. Below $50/month is too thin — one repair wipes out months of profit. See the full cash flow calculation guide for detailed expense breakdowns.

Run it: Cash Flow Calculator

Step 5: Check Property Tax Reassessment

This is the step most investors skip — and it costs them thousands.

When you buy a property, the county reassesses the tax based on your purchase price. A property currently taxed at $1,500/year on a $100,000 assessment may jump to $3,000/year when you buy it for $200,000.

How to check: Call the county assessor’s office or search their website. Look up the current assessed value and the local mill rate. Multiply your purchase price by the mill rate for the projected tax.

Kill signal: Post-sale property tax increase flips cash flow negative.

Step 6: Estimate Rehab Costs

If the property needs work, get accurate numbers before making an offer — not after.

- Walk the property with a contractor for a free estimate

- Use per-square-foot estimates: light rehab $15-25/sqft, medium $25-40/sqft, full gut $40-60+/sqft

- Add 15% contingency — always

- Check roof age, HVAC age, plumbing material, electrical panel amperage

Run it: Rehab Cost Estimator. Full breakdown: How Much Does It Cost to Rehab a House.

Kill signal: Rehab cost + purchase price exceeds 75% of ARV (for flips) or makes cash flow negative (for rentals).

Step 7: Verify Insurance Costs

Call an insurance broker and get a quote before making an offer. Properties in flood zones, hurricane-prone areas, or high-crime neighborhoods carry premiums 2-4x the normal rate.

What to ask for: Landlord dwelling policy with liability coverage. If planning Airbnb, request an STR-specific policy (costs 2-3x more). See the Airbnb income guide for STR insurance details.

Kill signal: Insurance exceeds 1% of property value per year in a non-coastal market.

Step 8: Check Vacancy Rate

High vacancy kills cash flow faster than any other factor. Research your target market before assuming a number.

- National average: 6.4% (U.S. Census Bureau)

- Strong markets (Cleveland, Indianapolis): 5-7%

- Soft markets: 8-12%

Run it: Vacancy Rate Calculator

Kill signal: Local vacancy above 10% without a clear turnaround thesis.

Step 9: Calculate Cash-on-Cash Return

This tells you whether your capital is working hard enough in this deal compared to alternatives.

Formula: Cash-on-Cash = Annual Cash Flow ÷ Total Cash Invested × 100

Total cash invested = down payment + closing costs + rehab + reserves.

| Cash-on-Cash | Action |

|---|---|

| 8%+ | Strong — proceed to final step |

| 4%–8% | Acceptable if appreciation potential exists |

| Below 4% | Capital earns more elsewhere — pass or renegotiate |

Run it: Cash-on-Cash Calculator

Step 10: Stress Test the Deal

The final step: break the deal on paper before real life breaks it for you.

The final step of the real estate deal analysis checklist: run three stress-test scenarios:

| Scenario | What to Change | What You Learn |

|---|---|---|

| Rent drops 10% | Reduce rent by 10% | Can you survive a soft market? |

| Vacancy doubles | Increase vacancy to 12-15% | Can you survive extended vacancy? |

| Rate increases 1% | Add 1% to interest rate | Can you survive a rate adjustment? |

If the deal survives all three checks on your real estate deal analysis checklist with positive (or near-positive) cash flow, it is resilient. If any single stress test flips it deeply negative, the deal is fragile.

Run all scenarios in the Rental Property Calculator or Compare Deals tool.

Real Estate Deal Analysis Checklist: Quick Reference

| # | Step | Pass | Kill |

|---|---|---|---|

| 1 | Verify rent | Matches 3+ comps | 20%+ above comps |

| 2 | Cap rate | 5%+ | Below 5% |

| 3 | DSCR | 1.0+ | Below 1.0 |

| 4 | Cash flow | $100+/unit/mo | Negative |

| 5 | Tax reassessment | Cash flow survives new tax | Flips negative |

| 6 | Rehab estimate | Within 75% ARV | Exceeds ARV margin |

| 7 | Insurance quote | Under 1% of value | 2x+ normal |

| 8 | Vacancy rate | Under 8% | Above 10% |

| 9 | Cash-on-Cash | 4%+ | Below 4% |

| 10 | Stress test | Survives 3 scenarios | Breaks under 1 scenario |

Worked Example: Screening a Memphis Duplex

Asking price $195,000. Two units renting at $900 and $850/month ($1,750 total).

| Step | Result | Pass? |

|---|---|---|

| 1. Rent verification | Comps show $850-$950 range — checks out | ✅ |

| 2. Cap rate | NOI $12,600 ÷ $195,000 = 6.5% | ✅ |

| 3. DSCR | $1,750 ÷ $1,380 PITIA = 1.27 | ✅ |

| 4. Cash flow | $1,750 − $625 expenses − $1,038 P&I = $87/mo per unit | ⚠️ thin |

| 5. Tax reassessment | Current $1,800/yr → projected $2,340 (+$540) | ✅ survives |

| 6. Rehab | $8,000 cosmetic (paint, flooring) | ✅ |

| 7. Insurance | $1,400/yr (0.7% of value) | ✅ |

| 8. Vacancy | Memphis metro: 7% | ✅ |

| 9. Cash-on-Cash | $2,088 ÷ $48,000 = 4.4% | ✅ marginal |

| 10. Stress test | Rent −10%: CF goes negative. Fragile. | ⚠️ |

The real estate deal analysis checklist shows this deal passes 8 of 10 steps but is fragile — a 10% rent drop kills cash flow. Worth pursuing only if you can negotiate the price down to $180,000 or below, which would improve cap rate to 7.0% and give a stress-test cushion.

Disclaimer

This article and the referenced calculators are for educational purposes only. Real estate deal analysis involves assumptions that may not reflect actual market conditions, property performance, or financing terms. Always verify data independently, consult licensed real estate professionals, inspectors, and financial advisors before making investment decisions. ArvCalc is not a broker, lender, or financial advisor.

The first step in any real estate deal analysis checklist is verifying rent, because every other metric depends on it. If rent is overstated, cap rate, DSCR, cash flow, and cash-on-cash return are all inflated. Always verify rent with at least three comparable listings before running any calculations.

Using a real estate deal analysis checklist, an initial screening (steps 1-4) takes 10-15 minutes per property and eliminates 80% of deals. Full underwriting (steps 5-10) takes 2-4 hours including phone calls to insurance brokers, county assessors, and contractors. Do the quick screen first to avoid wasting time on deals that fail basic metrics.

Target 5% minimum for stable markets and 7%+ for cash flow-focused investing. Midwest markets like Cleveland, Indianapolis, and Memphis offer 7-10% cap rates. Coastal and high-growth markets like Austin and Nashville may trade at 4-5% with lower cash flow but higher appreciation potential.

The final step of the real estate deal analysis checklist: run three stress-test scenarios: reduce rent by 10%, double your vacancy assumption (from 7% to 14%), and add 1% to the interest rate. If the deal remains cash-flow positive under all three scenarios, it is resilient. If any single scenario flips it deeply negative, the deal is fragile and one bad quarter could force you to sell at a loss.

Most investors target 8% or higher for buy-and-hold rentals. Returns of 4-8% are acceptable if the property offers appreciation or strategic value. Below 4% suggests the capital would earn more in alternative investments like index funds or REITs with less effort and risk.

Yes. Budget 8-10% for property management regardless of whether you self-manage. This ensures the deal works as an investment, not as a part-time job. If you scale to multiple properties or your situation changes, you will need professional management. A deal that only works with free owner labor is not a good investment.

When running a real estate deal analysis checklist, the three most common deal killers are: property tax reassessment (the tax jumps 40-100% after purchase), negative cash flow at realistic vacancy rates (8% vs the 5% the seller assumed), and rehab costs exceeding the budget by 30%+ due to hidden structural or system issues discovered after the offer is accepted.

Leave a Reply