What Is Real Estate Depreciation?

Real estate depreciation is a tax deduction that lets you write off the cost of your rental property over 27.5 years — even though the property is probably gaining value, not losing it. It is one of the biggest tax advantages of owning investment property, and most landlords either underuse it or do not understand it at all.

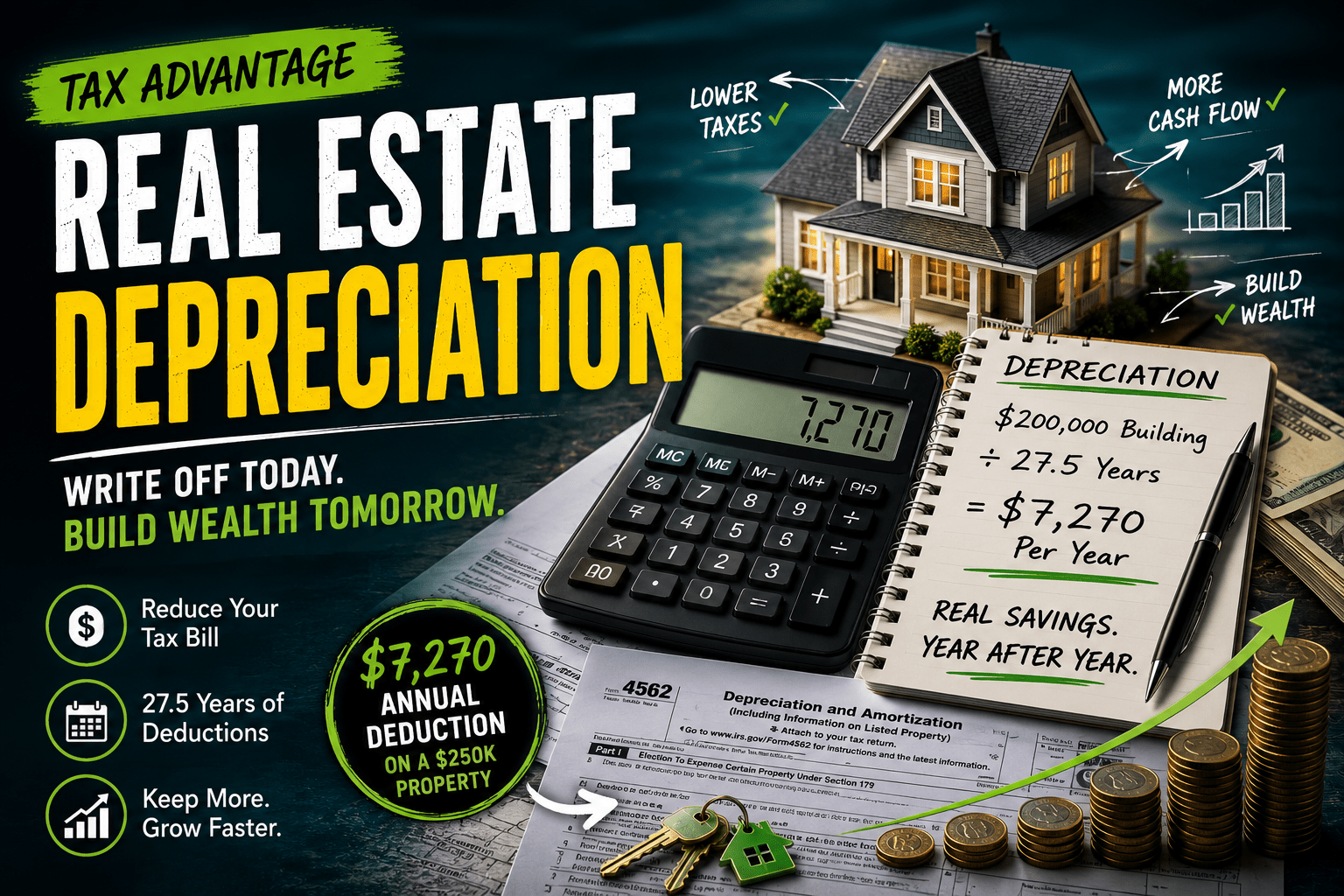

On a $250,000 rental property, depreciation generates approximately $7,270 in annual tax deductions. At a 24% tax bracket, that saves $1,745 per year in real cash — money you keep because the IRS lets you pretend your building is losing value.

This guide explains how real estate depreciation works, how to calculate it, what cost segregation does, and the depreciation recapture tax you will owe when you sell. Use the free Depreciation Calculator to estimate your annual deduction.

How Real Estate Depreciation Works Step by Step

According to IRS Publication 946, the IRS considers rental buildings (not land) as assets that wear out over time. Even though your property may appreciate 3-4% per year, the tax code allows you to deduct a portion of the building’s cost every year as an “expense” — reducing your taxable rental income.

The formula:

Annual Depreciation = (Property Value − Land Value) ÷ 27.5 years

Land cannot be depreciated because it does not “wear out.” You must separate the building value from the land value. Typical split: 75-85% building, 15-25% land. Your county tax assessment usually shows this breakdown. The IRS Publication 527 covers depreciation rules specific to residential rental property.

Worked Example: Memphis Duplex

Sarah buys a duplex in Memphis for $210,000. County assessment shows 80% building ($168,000) and 20% land ($42,000).

| Item | Value |

|---|---|

| Purchase price | $210,000 |

| Land value (20%) | $42,000 |

| Building value (80%) | $168,000 |

| Annual depreciation ($168K ÷ 27.5) | $6,109 |

| Monthly depreciation | $509 |

| Tax savings at 24% bracket | $1,466/year |

Sarah deducts $6,109 from her rental income every year for 27.5 years — a total of $168,000 in deductions over the life of the property. This is not actual money spent — it is a paper loss that reduces her tax bill while her property appreciates in the background.

Run your numbers: Depreciation Calculator

How Real Estate Depreciation Reduces Your Tax Bill

Depreciation directly reduces your taxable rental income. Here is how it works in practice:

| Line Item | Without Depreciation | With Depreciation |

|---|---|---|

| Gross rental income | $25,200 | $25,200 |

| Operating expenses | −$8,400 | −$8,400 |

| Mortgage interest | −$10,500 | −$10,500 |

| Depreciation | $0 | −$6,109 |

| Taxable income | $6,300 | $191 |

| Tax owed (24%) | $1,512 | $46 |

| Tax savings | — | $1,466 |

Without depreciation, Sarah owes $1,512 in tax on her rental income. With depreciation, she owes $46. The property puts the same cash in her pocket either way — depreciation just lets her keep more of it.

In many cases, depreciation creates a paper loss even when the property cash flows positively. Sarah’s property generates $200/month in real cash flow, but shows a $191 “profit” on her tax return — effectively paying almost zero tax on her rental income.

Real Estate Depreciation: Cost Segregation Strategy

Standard depreciation spreads the deduction evenly over 27.5 years. Cost segregation front-loads it by separating the building into components with shorter depreciation schedules:

| Component | Depreciation Period | Examples |

|---|---|---|

| Building structure | 27.5 years | Walls, roof, foundation |

| Land improvements | 15 years | Landscaping, parking, fencing, sidewalks |

| Personal property | 5-7 years | Appliances, carpet, cabinets, fixtures |

| Bonus depreciation (2026) | Year 1 (40%) | Qualifying 5/7/15-year property |

A cost segregation study on a $210,000 duplex might reclassify $40,000 from 27.5-year to 5-15 year property. At 40% bonus depreciation in 2026, that produces a $16,000 first-year deduction instead of $1,455. The tax savings difference is significant — especially for high-income investors.

When cost segregation makes sense: Properties above $200,000 in value, investors in the 32%+ tax bracket, and those with Real Estate Professional status (750+ hours/year) who can use losses against other income.

Cost: A professional cost segregation study runs $3,000-$8,000. For a $300,000+ property in a high tax bracket, the first-year tax savings typically exceed the study cost by 3-5x.

Real Estate Depreciation Recapture: The Tax at Sale

Here is the catch: when you sell the property, the IRS “recaptures” the depreciation you claimed at a 25% tax rate. This is on top of your capital gains tax.

Example: Sarah Sells After 10 Years

| Item | Amount |

|---|---|

| Sale price | $285,000 |

| Original purchase | $210,000 |

| Capital gain | $75,000 |

| Depreciation claimed (10 years × $6,109) | $61,090 |

| Capital gains tax (15%) | $11,250 |

| Depreciation recapture (25%) | $15,273 |

| Total tax at sale | $26,523 |

Sarah saved $14,660 in taxes over 10 years through depreciation ($1,466 × 10) but owes $15,273 in recapture at sale. So did depreciation actually help?

Yes — for two reasons:

- Time value of money. She had $1,466 extra per year for 10 years. Invested at 8%, that $14,660 in tax savings grew to approximately $21,200. She kept the growth — the IRS only recaptures the original $15,273.

- 1031 exchange defers recapture. If Sarah does a 1031 exchange instead of selling for cash, she defers both capital gains AND depreciation recapture. The 1031 Exchange Calculator models total tax deferral. See also 7 strategies to avoid capital gains tax.

5 Real Estate Depreciation Mistakes Landlords Make

1. Not claiming depreciation at all. The IRS charges recapture on depreciation you could have claimed — even if you didn’t. If you own a rental and are not taking depreciation, you are paying tax twice: once on the income you didn’t offset, and again on the recapture you never received. Start claiming immediately.

2. Depreciating land. Only the building depreciates, not the land. If your county assessment does not separate them, use 75-80% building as a conservative estimate. Depreciating land triggers IRS scrutiny.

3. Forgetting to add improvements to the depreciable basis. A $15,000 roof replacement adds $15,000 to your depreciable basis — an extra $545/year in deductions for 27.5 years. Track every capital improvement. Use the Rehab Cost Estimator to categorize repairs vs improvements.

4. Not considering cost segregation. Straight-line depreciation over 27.5 years is the default. Cost segregation can 3-5x your first-year deduction — but only works if you do it proactively. It can also be done retroactively through a “look-back” study.

5. Ignoring recapture in the sale analysis. Many investors calculate flip or sale profit without budgeting for 25% depreciation recapture. On 10 years of depreciation, recapture can be $15,000-$30,000. Always include it in your exit analysis. The Capital Gains Tax Calculator includes recapture.

Depreciation and Your NOI

Depreciation is NOT included in Net Operating Income. NOI measures actual cash expenses — depreciation is a non-cash tax deduction. However, depreciation affects your taxable income and therefore your actual after-tax return.

When analyzing deals, calculate NOI without depreciation, then add depreciation separately to your tax projections. The NOI improvement guide covers operational changes; depreciation is a tax strategy, not an operations strategy.

For total return including depreciation benefits, use the IRR Calculator — it factors in tax savings from depreciation over the hold period. See the IRR guide for how depreciation fits into total return analysis.

Real Estate Depreciation Schedule by Property Type

Not all real estate depreciates at the same rate. The IRS assigns different recovery periods based on property type:

| Property Type | Recovery Period | Annual Rate | Example |

|---|---|---|---|

| Residential rental (1-4 units) | 27.5 years | 3.636% | $200K building = $7,273/yr |

| Residential rental (5+ units) | 27.5 years | 3.636% | Same rate as small residential |

| Commercial property | 39 years | 2.564% | $500K building = $12,821/yr |

| Land improvements | 15 years | 6.667% | Parking lot, fence, landscaping |

| Appliances, carpet, cabinets | 5-7 years | 14-20% | $10K appliance package = $2,000/yr |

Residential investors get the better deal — 27.5 years versus 39 for commercial. This is one reason many investors prefer residential multifamily over commercial for tax efficiency.

Real Estate Depreciation and Your Investment Return

Depreciation does not appear in cash flow or NOI calculations — those track actual money. But depreciation significantly affects your after-tax return, which is what you actually keep.

Consider two identical properties producing $3,000/year in pre-tax cash flow:

| Scenario | Pre-Tax Cash Flow | Depreciation Deduction | Taxable Income | Tax (24%) | After-Tax Cash Flow |

|---|---|---|---|---|---|

| No depreciation (stocks) | $3,000 | $0 | $3,000 | $720 | $2,280 |

| With depreciation (rental) | $3,000 | $7,273 | -$4,273 (loss) | $0 | $3,000 |

The rental investor keeps $720 more per year — 31% more after-tax cash flow on the same pre-tax income. Over 10 years, that is $7,200 in additional retained wealth. This is why real estate investors say “you don’t pay taxes on rental income” — technically you do, but depreciation often eliminates or reduces it to near zero.

Factor this into your total return analysis: IRR Calculator. For strategies to reduce tax further when you sell, see 7 ways to avoid capital gains tax.

When to Start and Stop Depreciating

Start: Depreciation begins when the property is “placed in service” — the day it is available for rent, not the day you buy it. If you buy on January 15 and list for rent on February 1, depreciation starts February 1.

Stop: Depreciation ends when you sell the property, convert it to personal use, or have fully depreciated the building value (after 27.5 years). If you sell after 10 years, you only claimed 10/27.5 of the total.

Partial year: The IRS uses the mid-month convention — if you place the property in service any day in March, you get 9.5 months of depreciation in year 1 (mid-March through December). According to IRS Form 4562 instructions, residential rental property uses the mid-month convention under MACRS (Modified Accelerated Cost Recovery System).

Disclaimer

This article is for educational purposes only and does not constitute tax, legal, or financial advice. Tax laws regarding depreciation, cost segregation, and recapture are complex and change frequently. The examples provided use simplified assumptions that may not reflect your specific tax situation. Consult a licensed CPA, tax attorney, and financial advisor before making decisions based on depreciation strategies. ArvCalc is not a CPA, tax advisor, or attorney.

Real estate depreciation allows you to deduct the cost of your rental building (not land) over 27.5 years. Each year, you subtract 1/27.5 of the building value from your taxable rental income. On a property with $200,000 in building value, that is $7,273 per year in tax deductions — reducing your tax bill by $1,745 at a 24% tax rate. The property can be appreciating in actual value while you claim it is losing value for tax purposes.

Annual depreciation equals building value divided by 27.5. On a $250,000 property with 80% building value ($200,000), annual depreciation is $7,273. Over 27.5 years, you deduct the entire building value. Cost segregation can accelerate this by reclassifying components to 5, 7, or 15-year schedules — potentially producing $15,000-$30,000 in first-year deductions on the same property.

When you sell a rental property, the IRS taxes all depreciation you claimed (or could have claimed) at a 25% rate. This is called depreciation recapture. If you claimed $60,000 in total depreciation over your hold period, you owe $15,000 in recapture tax at sale — in addition to capital gains tax. Recapture can be deferred through a 1031 exchange.

Yes, for two reasons. First, the time value of money: you receive tax savings every year for 10-27.5 years, which you can invest. The compounded returns on those savings typically exceed the recapture tax. Second, a 1031 exchange defers recapture indefinitely — and if you hold until death, your heirs receive a stepped-up basis that eliminates recapture entirely.

Cost segregation is a tax strategy that reclassifies building components from 27.5-year depreciation to shorter schedules (5, 7, or 15 years), accelerating your deductions into the early years. It makes sense for properties above $200,000, investors in the 32%+ tax bracket, and those with Real Estate Professional status. A study costs $3,000-$8,000 and typically pays for itself 3-5x in first-year tax savings.

Yes. You can file Form 3115 (Change in Accounting Method) to claim all missed depreciation in the current year as a one-time catch-up deduction. This does not amend prior returns — it adjusts your current year. This is important because the IRS charges recapture on depreciation you could have claimed, whether you actually did or not. Consult a CPA to file the Form 3115 correctly.

Leave a Reply