The BRRRR strategy — Buy, Rehab, Rent, Refinance, Repeat — is a real estate investment method that lets you recycle your capital across multiple rental properties. Instead of locking up a down payment in each deal, you buy undervalued properties, force appreciation through renovation, and pull your cash back out through a cash-out refinance.

Sounds straightforward. Execution is where most investors get tripped up. Hard money rates above 11% in 2026, tighter appraisals, and high conventional rates at 7.5% make the math harder than it was three years ago. A BRRRR deal that looked easy on paper in 2021 might not pencil out today.

This guide breaks down every step of the BRRRR strategy with real 2026 numbers — so you can figure out whether a deal actually works before you spend money on it.

Run your own scenarios with our BRRRR Calculator as you read through each section.

How the BRRRR Strategy Works: Step by Step

Each letter in BRRRR represents a phase. Phases overlap in practice, but the financial logic follows a specific sequence.

Buy

You purchase a property below market value. Discounts usually come from distressed sellers, foreclosures, probate sales, or properties that need significant work. Investors typically finance this purchase with hard money loans — short-term, high-interest loans designed for exactly this scenario.

A hard money lender might cover 80% of the purchase price at 11-13% interest with 2-3 origination points. You bring the remaining 20% plus closing costs. On a $150,000 property, that means roughly $30,000-$40,000 out of pocket before rehab even starts.

Rehab

This is the value-add phase. You renovate the property to bring it up to the standard of comparable rentals in the area. Your goal is forced appreciation — the property should appraise significantly higher after renovation than what you paid for it plus rehab costs.

Two things trip up first-time BRRRR investors here. First, rehab budgets almost always run over. A good rule of thumb is to add 15% contingency on top of your contractor’s estimate. Second, the timeline matters because you are paying hard money interest every month. At 12%, that is roughly $1,500/month on a $150,000 loan. Every extra month eats directly into your profit.

Rent

Once the renovation is done, you place a tenant and start collecting rent. This step serves two purposes. It generates income that covers your holding costs while you wait for the seasoning period to pass, and it establishes the property as a performing rental — which is what the conventional lender wants to see before approving a refinance.

Most lenders require a 3-6 month seasoning period between purchase and refinance. Fannie Mae guidelines specify a minimum six-month ownership for cash-out refinances. Some portfolio lenders will refinance with no seasoning, but they usually charge higher rates or fees to compensate.

Refinance

This is where the capital recycling happens. You refinance the property from the short-term hard money loan into a long-term conventional mortgage. The key part: the new loan is based on after-repair value (ARV), not what you originally paid.

BRRRR math gets interesting here. If you bought a property for $150,000, spent $40,000 on rehab, and the ARV comes back at $250,000, a 75% LTV refinance gives you a new loan of $187,500. That pays off the hard money loan ($150,000 principal) and puts $37,500 minus closing costs back in your pocket.

Your total cash invested might have been $35,000-$45,000 (down payment on hard money + rehab costs that weren’t financed + holding costs + points). If the refi proceeds cover that amount, you’ve achieved full capital recovery — your money is back, and you still own a cash-flowing rental.

Repeat

With your capital returned, you do it again with the next property. This is what makes the BRRRR strategy different from traditional buy-and-hold investing. Instead of tying up $40,000 per property, you recycle the same capital across multiple deals. Three BRRRR deals with full capital recovery means you own three rentals for roughly the same out-of-pocket cost as one traditional purchase.

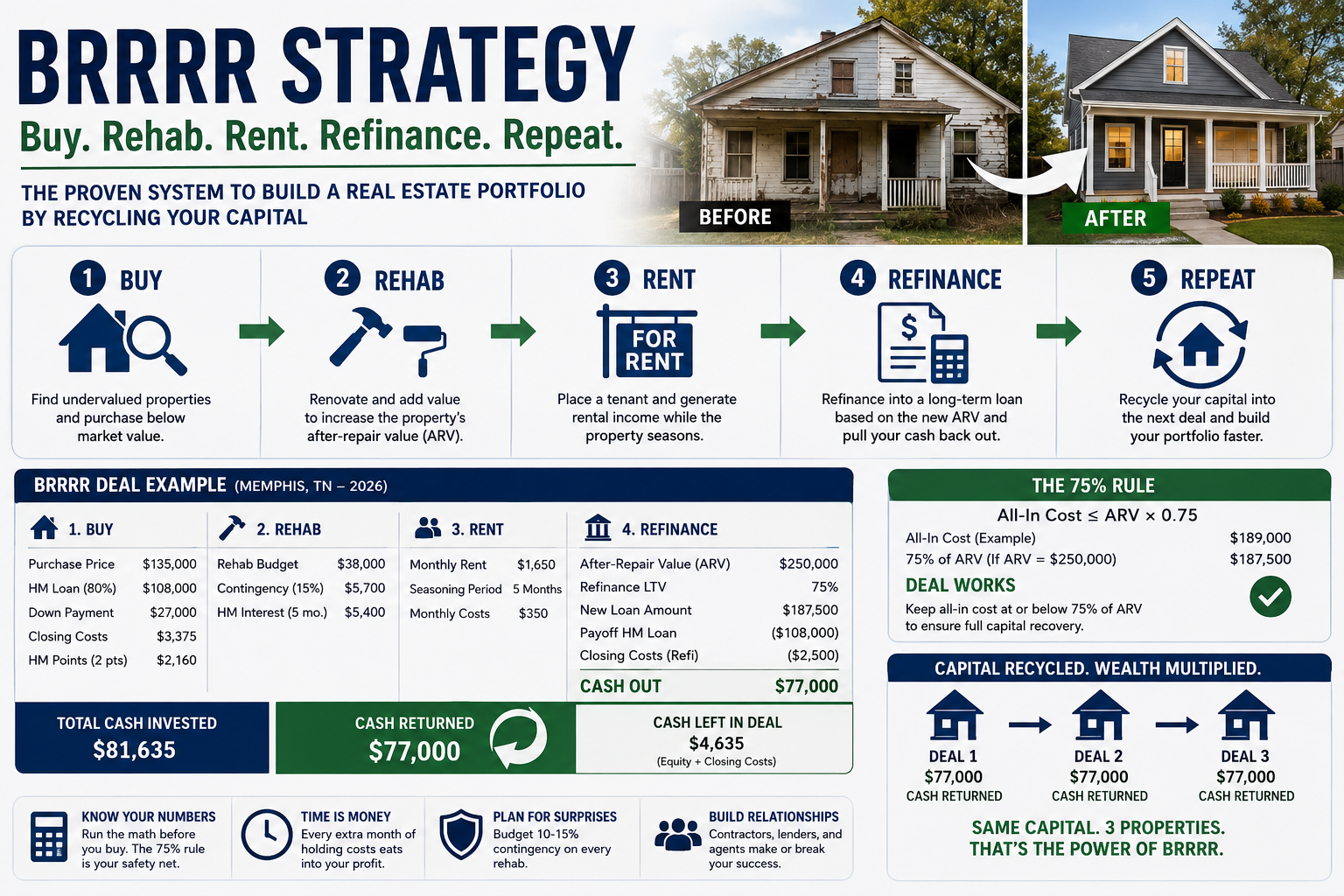

The 75% Rule for BRRRR

Every experienced BRRRR investor knows the 75% rule. It is the single most important screening filter for BRRRR deals, and it is different from the 70% rule used for flips.

The logic: if your all-in cost (purchase + rehab + closing + holding costs) stays at or below 75% of the ARV, you can theoretically recover all your capital through a 75% LTV refinance.

75% Rule formula:

All-In Cost ≤ ARV × 0.75

Example with numbers:

| Cost Item | Amount |

|---|---|

| Purchase price | $140,000 |

| Rehab | $35,000 |

| Closing costs | $4,200 |

| Holding costs (5 months at 12% HM) | $7,000 |

| HM points (2 points) | $2,800 |

| All-in cost | $189,000 |

For full capital recovery, you need: $189,000 ÷ 0.75 = ARV of at least $252,000

If the property appraises at $260,000 after rehab, you are within the 75% rule and the math works. If it appraises at $230,000, you are leaving money in the deal — specifically about $16,500.

This is fundamentally different from the 70% rule for flipping. One protects flip profit margin. One targets capital recovery through refinancing. Mixing them up leads to bad purchase decisions.

BRRRR Deal Walkthrough: 2026 Numbers

Numbers from an actual market — Memphis, Tennessee. Not a hypothetical.

Phase 1: Buy + Rehab

| Item | Amount | Notes |

|---|---|---|

| Purchase price | $135,000 | 3-bed SFR, outdated kitchen/bath, needs roof patch |

| Hard money loan | $108,000 | 80% LTC at 12%, 2 points, interest-only |

| Down payment (HM) | $27,000 | 20% of purchase |

| HM origination points | $2,160 | 2 points on $108K |

| Closing costs | $3,375 | 2.5% of purchase |

| Rehab budget | $38,000 | Kitchen $12K, bath $8K, flooring $6K, roof $5K, paint/misc $7K |

| Contingency (15%) | $5,700 | 15% of rehab |

| HM interest during hold | $5,400 | 5 months at $1,080/mo |

| Total cash invested | $81,635 | Down + closing + rehab + contingency + points + interest |

Note: rehab is paid out of pocket here because the hard money loan only covered 80% of the purchase. Some HM lenders will cover purchase + rehab — in that case your cash invested drops significantly.

Phase 2: Refinance

| Item | Amount |

|---|---|

| ARV after rehab | $215,000 (3 comparable renovated sales within 0.5 miles) |

| Refi terms | 75% LTV at 7.5%, 30-year fixed |

| New loan amount | $161,250 |

| HM payoff (principal only) | −$108,000 |

| Refi closing costs (2.5%) | −$4,031 |

| Refi proceeds | $49,219 |

| Capital left in deal | $32,416 ($81,635 − $49,219) |

You did not achieve full capital recovery. You have $32,416 still in this deal. That is reality in 2026 — the “infinite return” deals that BRRRR YouTube channels promote are rare at current rates and valuations.

Phase 3: Year 1 Rental Performance

| Line Item | Annual |

|---|---|

| Monthly rent | $1,550/mo ($18,600/yr) |

| Vacancy (7%) | −$1,302 |

| Effective gross income | $17,298 |

| Property tax | −$945 |

| Insurance | −$675 |

| Property management (8%) | −$1,384 |

| Maintenance | −$1,350 |

| NOI | $12,944 |

| Debt service ($1,127/mo) | −$13,524 |

| Year 1 cash flow | −$580 |

| DSCR | 0.96 |

Cash flow is slightly negative in Year 1. This is common in 2026 BRRRR deals at 7.5% rates. What saves this deal is appreciation + equity buildup + rent growth. In Year 2 with a 3% rent increase, this property crosses into positive cash flow territory.

Is this a good BRRRR? Depends on your goals. You have $32,416 in the deal and own a property worth $215,000 with a $161,250 mortgage — that is $53,750 in equity. Cash-on-cash on the remaining capital is thin, but total return including equity is strong.

When the BRRRR Strategy Works Best

The BRRRR strategy is not universal. It works in specific conditions:

Markets with a wide spread between distressed and retail prices. If you can buy at 60-65% of ARV, the 75% rule works naturally. In markets where distressed properties still sell at 85-90% of ARV (like much of California), the math almost never pencils out.

Markets with reliable rent-to-price ratios above 0.8%. Post-refi cash flow depends on rent covering the new mortgage plus expenses. Midwest and Southeast markets (Memphis, Cleveland, Indianapolis, Birmingham) offer ratios above 1.0%. Coastal markets rarely break 0.5%.

Rehabs under $50,000 on properties under $200,000. When rehab costs balloon relative to purchase price, holding costs eat into the margin. A $100,000 rehab on a $200,000 property with 12% hard money interest adds $2,000/month in holding costs alone.

ARV appraisals that hold up. Everything hinges on the post-rehab appraisal coming in at or above your target. If the appraiser uses comps that are 10% lower than what you expected, the refi proceeds drop and you leave more capital in the deal. This is the #1 risk in BRRRR.

5 BRRRR Strategy Mistakes That Cost Real Money

1. Overestimating ARV. Pull 3-5 recent comps of actually renovated properties within half a mile. Use the median, not the highest. Every $10,000 of ARV overestimation means roughly $7,500 less in refi proceeds.

2. Underestimating rehab timeline. Budget 15% contingency on costs and add 2 months to the contractor’s timeline. At hard money rates, each extra month costs $1,000-$2,500 in interest that comes straight out of your returns.

3. Ignoring post-refi cash flow. Getting your capital back means nothing if the property bleeds cash every month after refinancing. Run the full rental analysis at current conventional rates before committing to the purchase. Use a rental property calculator alongside the BRRRR analysis.

4. Confusing the 75% rule with the 70% rule. Flip investors use the 70% rule (Max Offer = ARV × 0.70 − Rehab). BRRRR investors use the 75% rule (All-In Cost ≤ ARV × 0.75). Using the wrong rule means either overpaying or passing on workable deals.

5. Assuming “infinite return” is normal. Social media makes every BRRRR strategy deal look like a guaranteed capital recovery plus extra. In 2026, with hard money at 12% and conventional at 7.5%, most BRRRR deals leave $15,000-$40,000 in the property. That is still a good outcome — just not the YouTube fantasy.

BRRRR Strategy vs Fix-and-Flip: Which Makes More Sense?

Both strategies start the same way — buy low, renovate, create value. They diverge at the exit.

A flipper sells the property and takes profit as a lump sum. A BRRRR investor refinances and holds. Financially it comes down to this: flipping generates immediate cash but triggers short-term capital gains tax (taxed as ordinary income, often 25-37%). BRRRR defers the tax event and builds long-term wealth through equity, rent, and depreciation.

In 2026, flipping margins have compressed because of high holding costs. A deal that produces $25,000 net flip profit might produce $15,000-$20,000 after tax. That same property held as a BRRRR rental builds $5,000-$8,000 in equity per year through mortgage paydown alone, plus appreciation, plus rent income, plus a depreciation tax deduction of roughly $4,000-$5,000 annually.

Your choice comes down to whether you need cash now or wealth later. Many investors start with flips to build capital, then switch to BRRRR once they have enough reserves to hold properties long-term.

BRRRR Strategy Financing: Hard Money + Refinance

A BRRRR deal requires two separate loans — and each one has terms that affect the deal differently.

Phase 1: Hard Money Loan

Hard money lenders care primarily about the property and the project, not your W-2 income. Illustrative terms:

| Term | Illustrative Range |

|---|---|

| Loan-to-cost | 75-85% of purchase (some cover purchase + rehab) |

| Interest rate | 11-13% |

| Origination points | 1.5-3 points |

| Loan term | 6-18 months |

| Payments | Interest-only (principal due as balloon at refi) |

Biggest variable: whether the lender covers rehab costs. If yes, your out-of-pocket drops dramatically but the loan amount — and interest payments along with it — increase. Run both scenarios through the hard money calculator before choosing.

Phase 2: Conventional Refinance

After the seasoning period (3-12 months depending on the lender), you refinance into a conventional or DSCR loan:

| Term | Illustrative Range |

|---|---|

| LTV | 70-80% of appraised value (75% standard for investment) |

| Rate | 7-8% conventional; DSCR loans 0.5-1% higher |

| Loan term | 30-year fixed (most common) |

| Closing costs | 2-3% of new loan amount |

DSCR loans have become popular for BRRRR because they qualify based on property income rather than personal income. If the property’s DSCR ratio is above 1.20-1.25, most DSCR lenders will approve regardless of how many properties you own.

Best Markets for the BRRRR Strategy in 2026

The BRRRR strategy works best where you can buy cheap, renovate reasonably, and rent at solid ratios. Investors are finding workable deals right now:

| Market | Purchase Range | Rent Range | Property Tax | Rent-to-Price | Notes |

|---|---|---|---|---|---|

| Memphis, TN | $120-200K | $1,100-1,700 | ~0.7% | 0.9-1.1% | Strong rental demand, competitive rehab costs |

| Cleveland, OH | $80-150K | $1,000-1,500 | ~1.5% | 1.0-1.3% | Lowest entry, higher tax offset by low prices |

| Indianapolis, IN | $130-210K | $1,000-1,500 | ~0.9% | 0.7-0.9% | Population growth, balanced market |

| Birmingham, AL | $70-130K | $900-1,200 | ~0.5% | 1.0-1.3% | Lowest entry in US, wide distressed-retail spread |

Markets to avoid for the BRRRR strategy: anywhere with median home prices above $400K, property tax rates above 2%, or rent-to-price ratios below 0.6%. Most of California, the Northeast corridor, and Pacific Northwest fall into this category.

How to Use the BRRRR Calculator

The BRRRR Calculator runs the complete two-phase analysis. Each section covers:

Purchase inputs: property price, closing costs, hard money terms (LTC, rate, points), and whether the HM loan covers rehab.

Rehab inputs: renovation budget, contingency percentage, seasoning period in months.

Refinance inputs: ARV (your estimate of post-rehab value), conventional loan LTV, rate, term, and closing costs.

Rental inputs: monthly rent, vacancy rate, property tax, insurance, PM fee, maintenance.

Two primary metrics come out of the analysis: Capital Left in Deal (how much of your cash is still tied up after refinancing) and Post-Refi Cash-on-Cash Return (annual return on that remaining capital). It also checks the 75% rule and shows post-refi DSCR.

Three modes are available: standard analysis, find the required ARV for full capital recovery, and find the maximum purchase price that keeps you within the 75% rule.

What This Calculator Does Not Cover

This calculator focuses on one question: how much money stays in the deal after refinancing, and what return does that remaining capital earn in Year 1?

It does not project multi-year performance. For a 5-10 year hold analysis including appreciation, rent growth, and mortgage paydown, use the Rental Property Calculator with your post-refi numbers.

It does not calculate tax implications. BRRRR has favorable tax treatment — rental income is offset by depreciation, and refinance proceeds are generally not treated as taxable events (consult your CPA). But the specifics depend on your tax situation. Use the Depreciation Calculator for annual deduction estimates and consult a CPA for your specific scenario.

All projections are before-tax. Actual after-tax returns vary based on your marginal rate, depreciation schedule, and state tax laws.

Frequently Asked Questions

What is a good DSCR for a BRRRR refinance?

Most DSCR lenders require a minimum of 1.20-1.25x for investment property refinances. Below 1.0 means the rent does not cover the mortgage — the deal loses money monthly. Between 1.0 and 1.2, some lenders will approve but at higher rates or with larger down payments.

How long do I have to wait before refinancing a BRRRR property?

Seasoning periods vary by lender. Conventional lenders typically require 6-12 months of ownership before allowing a cash-out refinance based on a new appraisal. Some portfolio lenders and DSCR lenders offer shorter seasoning (3 months or even none), but these come with rate premiums.

Can I BRRRR with no money down?

Technically, if a hard money lender covers 100% of purchase and rehab costs, your only cash outlay is holding costs, points, and closing costs. But true zero-down BRRRR is rare. Most investors need $20,000-$50,000 in available capital per deal for the portions that hard money does not cover.

What happens if the appraisal comes in low?

You leave more capital in the deal than planned. If ARV appraises at $200K instead of $250K, your 75% LTV refi gives you $150K instead of $187.5K — that is $37,500 less in proceeds. You can either accept the lower proceeds, pay for a second appraisal (sometimes values differ), or wait for market appreciation and refinance later.

Is the BRRRR strategy still worth it in 2026 with high rates?

It depends on the market and the deal. The infinite-return BRRRR deals from 2020-2021 (when rates were 3-4%) are mostly gone. But leaving $20,000-$35,000 in a deal while owning a property worth $200,000+ is still a strong wealth-building outcome. The strategy works — the expectations just need to match current market reality.

Related Calculators

- BRRRR Calculator — Run the full buy-rehab-rent-refinance analysis

- BRRRR Refinance Calculator — Focus on the refinance step and capital recovery

- ARV Calculator — Estimate after-repair value using comparable sales

- Rental Property Calculator — Multi-year hold analysis after BRRRR refinance

- DSCR Calculator — Check if the deal qualifies for a DSCR refinance

- Hard Money Loan Calculator — Compare hard money costs and terms

- Fix & Flip Calculator — Compare BRRRR hold vs flip sale

Disclaimer: This article is for educational purposes only and does not constitute financial, investment, legal, or tax advice. Real estate investing involves significant risk, including the potential loss of capital. All numbers, rates, and market data referenced are illustrative examples based on general 2026 conditions and may not reflect your specific situation. Refinance proceeds and tax treatment depend on individual circumstances — consult a qualified CPA and real estate attorney before making any investment decisions.

Leave a Reply