How to Flip a House: What Beginners Need to Know

House flipping sounds simple — buy cheap, renovate, sell high. In practice, most first-time flippers either lose money or earn less than minimum wage for months of stressful work. The difference between a profitable flip and a disaster comes down to three things: buying at the right price, controlling rehab costs, and selling fast.

This guide covers the entire flipping process from finding deals to closing the sale, with real numbers at every step. No theory — just the math, the timeline, and the mistakes that cost beginners the most.

Run your flip numbers with the free Fix-and-Flip Calculator before making any offer.

Step 1: Learn the Numbers Before You Spend a Dollar

Every flip has the same financial structure. Memorize these five cost categories — they determine whether you make money or lose it.

| Cost Category | Typical % | On a $200K ARV Flip |

|---|---|---|

| Purchase price | 50-65% of ARV | $100,000-$130,000 |

| Rehab costs | 15-25% of ARV | $30,000-$50,000 |

| Holding costs (4-6 months) | 4-8% of ARV | $8,000-$16,000 |

| Selling costs (commission + closing) | 8-10% of ARV | $16,000-$20,000 |

| Profit | 10-15% of ARV | $20,000-$30,000 |

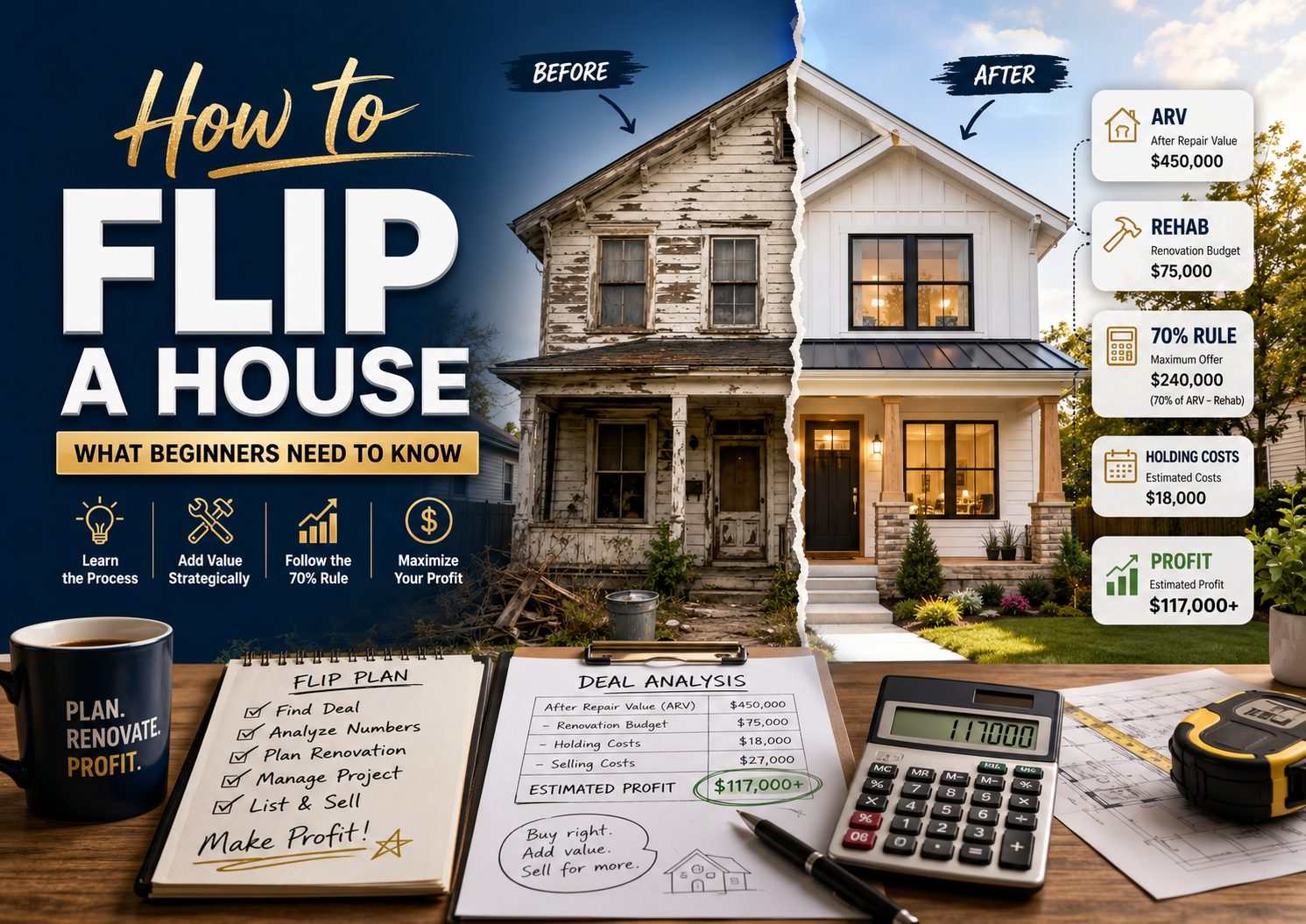

If your purchase + rehab + holding + selling exceeds 85% of ARV, there is no profit left. This is why the 70% rule exists — it ensures enough margin for costs plus profit.

The 70% Rule: Maximum Offer = ARV × 70% − Rehab Costs

On a $200K ARV property needing $40K rehab: $200,000 × 0.70 − $40,000 = $100,000 max offer. Use the 70% Rule Calculator for instant results.

Step 2: Find the Right Property

The best flip candidates share three traits: below-market price, cosmetic problems (not structural), and strong comparable sales nearby.

Where to Find Flip Properties

| Source | Typical Discount | Competition | Best For |

|---|---|---|---|

| MLS (listed properties) | 5-15% below ARV | High | Beginners — easy access |

| Wholesalers | 20-30% below ARV | Medium | Pre-screened deals, fast |

| Foreclosures / REO | 15-30% below ARV | Medium | Bank-owned, negotiable |

| Driving for dollars | 25-40% below ARV | Low | Off-market, best margins |

| Direct mail | 20-35% below ARV | Low | Motivated sellers |

| Auctions | 20-40% below ARV | Variable | Experienced only — risks |

For your first flip, stick to MLS or wholesaler deals. Off-market strategies require marketing spend and experience to evaluate deals under pressure.

What to Look For

Good flip candidates: Ugly cosmetics (dated kitchen, worn carpet, bad paint, overgrown yard), solid structure, good neighborhood with recent comparable sales above $150K.

Bad flip candidates: Foundation problems, mold, termite damage, flood zone, declining neighborhood, no comparable sales. These eat profit through unexpected costs and long timelines.

Before making an offer, estimate ARV using comparable sales. The ARV guide walks through the comp analysis process. Use the ARV Calculator to run the numbers.

Step 3: Finance the Deal

| Loan Type | Down Payment | Rate | Timeline | Best For |

|---|---|---|---|---|

| Hard money | 10-20% | 10-14% | 6-12 month term | Most flippers — fast close |

| Private money | Negotiable | 8-12% | Flexible | Relationship-based |

| Cash | 100% | 0% | N/A | No carrying costs, fastest |

| HELOC | 0% (equity) | 7-9% | Revolving | Using primary home equity |

| Conventional (rare for flips) | 15-25% | 6.5-7.5% | 30-45 day close | Only if holding 12+ months |

Most first-time flippers use hard money loans. They close in 7-14 days (vs 30-45 for conventional), fund 80-90% of purchase + 100% of rehab, and are designed for short-term holds. The cost: 2-4 points upfront plus 10-14% annual interest. Model your financing costs: Hard Money Loan Calculator.

According to ATTOM Data, the average flip in 2026 takes 162 days from purchase to sale. At 12% hard money rate on a $150,000 loan, that is $8,100 in interest alone. Every month over budget costs $1,500.

Step 4: Manage the Rehab

Rehab is where most flips go wrong. Budget overruns and timeline delays are the two biggest profit killers.

Rehab Budget by Scope

| Scope | Cost/Sq Ft | Timeline | Typical Items |

|---|---|---|---|

| Light cosmetic | $15-25 | 2-4 weeks | Paint, flooring, fixtures, landscaping |

| Medium rehab | $25-40 | 4-8 weeks | Kitchen, bathroom, some drywall, electrical |

| Full gut | $40-60+ | 8-16 weeks | Everything — structure, plumbing, HVAC |

For your first flip, target light-to-medium rehab. Full gut renovations carry too much risk for beginners — hidden problems multiply costs. Budget rehab line by line with the Rehab Cost Estimator. See the rehab cost breakdown for room-by-room pricing.

The 15% rule: Add 15% contingency to every rehab budget. On a $35,000 rehab, set aside $5,250 extra. In 50+ flips, fewer than 10% come in under budget.

3 Contractor Rules for First-Time Flippers

1. Get 3 bids. The lowest bid is almost never the best. The cheapest contractor who takes 8 months costs more in holding costs than a mid-price contractor who finishes in 10 weeks.

2. Never pay more than 50% upfront. Structure payments: 30% at start, 30% at midpoint, 30% at completion, 10% at final walkthrough. This keeps the contractor motivated to finish.

3. Get everything in writing. Scope of work, materials, timeline, payment schedule, change order process. Verbal agreements cost thousands in disputes.

Step 5: Sell the Property

Your flip is only profitable when the property sells. Every month on market after rehab costs $1,500-$3,000 in holding costs.

Pricing strategy: Price at 95-98% of your ARV estimate. Aggressive pricing sells faster. A property that sells in 2 weeks at $195K beats one that sits 3 months at $205K — the holding costs eat the $10K difference.

Staging matters. Staged homes sell 30-50% faster and for 5-10% more than empty homes, according to the National Association of Realtors. Budget $2,000-$4,000 for professional staging or $500-$1,000 for virtual staging.

Agent commission: Budget 5-6% of sale price. On a $200K sale, that is $10,000-$12,000. Some flippers sell FSBO to save commission, but the average FSBO sells for 6% less than agent-listed properties — netting the same or less after the hassle.

Worked Example: Cleveland 3BR Flip

| Item | Amount |

|---|---|

| ARV (after repair value) | $165,000 |

| 70% Rule max offer ($165K × 0.70 − $35K) | $80,500 |

| Purchase price | $78,000 |

| Rehab | $35,000 |

| Contingency (15%) | $5,250 |

| Hard money (12%, 5 months on $113K) | $5,650 |

| Points (2 points) | $2,260 |

| Holding (taxes, insurance, utilities) | $3,200 |

| Purchase closing costs | $2,400 |

| Selling agent commission (5.5%) | $9,075 |

| Selling closing costs | $3,300 |

| Total costs | $144,135 |

| Profit | $20,865 |

| ROI | 46% (on $45K cash invested) |

$20,865 profit on 5 months of work. That is $4,173/month — solid for a first flip. But if rehab had gone $10K over budget or the property sat 3 extra months, profit would have dropped to $5,000 or less.

Run your own deal: Fix-and-Flip Calculator

5 Mistakes That Kill First-Time Flips

1. Paying too much. The profit is made at purchase, not at sale. If you pay above the 70% rule, you are gambling that everything goes perfectly — and on flips, it rarely does.

2. Underestimating rehab by skipping the contingency. A $35,000 rehab without contingency becomes $42,000 when the plumber finds galvanized pipes behind the wall. That $7,000 surprise comes directly out of your profit.

3. Holding too long. Every extra month costs $1,500-$3,000. A 3-month delay on a deal with $20K profit reduces it to $11K-$15K. Price aggressively, sell fast.

4. Over-improving. Granite countertops in a $120,000 neighborhood do not add proportional value. Match finishes to the neighborhood — the highest comp is your ceiling. Check with the ARV Calculator.

5. Not knowing your exit before you buy. Know your ARV, your buyer pool, and your days-on-market before closing. If comparable properties sit 90+ days, your holding costs will eat your margin. Check the deal screening guide before making offers.

Flip vs BRRRR: Which Strategy Is Better?

| Factor | Flip | BRRRR |

|---|---|---|

| Goal | Quick profit | Build portfolio |

| Capital recycled? | Yes (at sale) | Yes (at refinance) |

| Passive income | No — one-time profit | Yes — monthly cash flow |

| Tax treatment | Ordinary income (up to 37%) | Capital gains (15-20%) if held 12+ months |

| Risk | Market timing, rehab overruns | Appraisal risk, tenant risk |

| Best for | Building capital fast | Building long-term wealth |

Many investors start with flips to build capital, then transition to BRRRR to build a portfolio. The BRRRR Calculator models the refinance step. For tax implications of each strategy, see the capital gains tax guide.

Disclaimer

This article is for educational purposes only and does not constitute financial, investment, or real estate advice. House flipping involves significant risk including potential loss of capital. Actual results depend on purchase price, rehab costs, market conditions, financing terms, and execution. Consult licensed real estate professionals, contractors, and financial advisors before purchasing properties for flipping. ArvCalc is not a broker, contractor, or financial advisor.

With hard money financing, you need 10-20% of the purchase price as a down payment plus cash for closing costs, holding costs during rehab, and a contingency reserve. On a $100,000 purchase with $35,000 rehab, expect to need $35,000-$50,000 in total cash. Some flippers start with as little as $20,000 using high-leverage hard money loans, but this leaves minimal margin for error.

The average flip takes 5-6 months from purchase to sale. Light cosmetic rehabs can be completed and sold in 3-4 months. Full gut renovations often take 6-9 months. The timeline breaks down as: 1-2 weeks to close purchase, 4-12 weeks for rehab, 2-4 weeks to list and market, 4-8 weeks to find a buyer and close the sale.

Most experienced flippers target $20,000-$30,000 net profit per flip, or 10-15% of the after-repair value. On a $200,000 ARV property, that means $20,000-$30,000 after ALL costs. First-time flippers often earn less due to rehab overruns and longer timelines. Flips that produce less than $10,000 profit are generally not worth the risk and effort involved.

The 70% rule states that you should pay no more than 70% of the after-repair value minus rehab costs. For example: ARV $200,000 times 0.70 minus $40,000 rehab equals $100,000 maximum purchase price. The 30% margin covers selling costs (agent commission 5-6%), closing costs (3-5%), holding costs (4-8%), and your profit (10-15%).

Yes, but margins are thinner than in 2020-2021 due to higher interest rates (hard money at 10-14%) and increased rehab costs. Successful flippers in 2026 focus on properties with strong cosmetic value-add potential in stable neighborhoods with quick sale times. The deals that work are the ones where purchase price is at or below the 70% rule — which requires patience and deal flow to find.

Flipping builds capital fast (one-time profit per deal) while rentals build long-term wealth (monthly income plus appreciation). Flips are taxed as ordinary income (up to 37%) while rentals held over 12 months qualify for lower capital gains rates (15-20%). Many investors start with 2-3 flips to build capital, then use the profits as down payments on rental properties for passive income.

Leave a Reply